Retiring at 62 With $1.4 Million Means Confronting a $14,200 Annual Gap Before Social Security Kicks In

The post Retiring at 62 With $1.4 Million Means Confronting a $14,200 Annual Gap Before Social Security Kicks In appeared first on 24/7 Wall St..

Retiring at 62 with $1.4 million sounds like a finish line. For a single retiree planning to wait until full retirement age of 67 to claim Social Security, it is actually the start of a five-year math problem most planning calculators gloss over. The portfolio can sustainably fund roughly $56,000 a year using the standard 4% rule. The desired lifestyle costs $70,200. That leaves a $14,200 annual gap every year until Social Security checks start arriving.

The Bridge Years Nobody Plans For

This scenario shows up constantly in retirement forums. On Suze Orman’s podcast, she has warned listeners repeatedly about the same trap: “you are taking your Social Security payments at 62, which for most of you is five years before your full retirement age. You are taking a serious hit on it, but that makes you feel secure.” The instinct to claim early is exactly what the gap years are designed to test.

The financial weight of those five years is bigger than it looks. Spending $70,200 while the portfolio can only safely produce $56,000 means pulling roughly $71,000 of extra principal over the bridge window. It is entirely manageable when treated as a planned bridge expense.

Here is the situation in one frame:

- Age & status: 62, single, retiring now

- Portfolio: $1.4 million

- Target spending: $70,200 per year (slightly above the U.S. per capita disposable income of $68,359 in Q1 2026)

- Sustainable withdrawal: $56,000 per year at 4%

- Core issue: Funding the $14,200 annual gap from age 62 to 67 without wrecking the portfolio or the future Social Security check

Why Claiming Early Is the Expensive Fix

The tempting move is to file at 62 and let Social Security plug the hole. The cost is permanent. Claiming at 62 when full retirement age is 67 locks in roughly a 30% reduction in monthly benefits for life. Benefits drop about 6.7% for each year claimed before FRA, and waiting past FRA adds roughly 8% per year up to age 70.

That math reframes the problem. A 30% haircut on a benefit collected for 20 or 30 years dwarfs a one-time $71,000 bridge draw from the portfolio. The right question is how to fund the bridge so the larger benefit stays intact.

Three Strategies That Actually Move the Needle

For most retirees in this exact position, the bridge bucket is the dominant strategy. The other two are accelerants.

- Carve out a five-year bridge bucket in cash and short Treasuries. The 5-year Treasury yields 4.29% as of June 8, 2026, with the 1-year at 3.85% and 3-year at 4.21%. A simple ladder covering the $14,200 annual gap (plus a buffer) removes equity-market timing risk for the years that matter most. With the Fed funds rate at 3.75% after 0.75% of cuts over the past year, locking in current yields has urgency.

- Run Roth conversions during the low-income bridge years. With no wages and no Social Security yet, taxable income drops sharply. Converting a slice of traditional IRA dollars into a Roth each year between 62 and 67, filling up the 12% or 22% bracket, reduces future required minimum distributions and creates tax-free withdrawal flexibility later. This window closes once Social Security and RMDs begin stacking.

- Reassess the withdrawal rate annually with guardrails. The 4% rule is a starting point. With CPI at 332.4 in April 2026, up 0.6% in a single month, and core PCE running near the Fed’s preferred measure, purchasing power can erode faster than budgets account for. A guardrail approach trims spending after a down market year and allows raises after a strong one.

What to Do This Quarter

Three concrete actions matter most:

- Build the bridge bucket before doing anything else. Move roughly $75,000 to $90,000 (the bridge total plus a cushion for inflation) into a 1-to-5 year Treasury or CD ladder. The 44 basis point pickup from the 1-year to the 5-year is meaningful on a five-year horizon.

- Map out Roth conversions year by year. The bridge years are the lowest-tax years a retiree may ever see again. National savings rates have fallen from 6.2% in Q1 2024 to 3.7% in Q1 2026, which means inflation is squeezing cash flow broadly. Tax efficiency is one of the few levers entirely under the retiree’s control.

- Resist the urge to claim at 62. The 30% permanent reduction is the single most expensive decision available in this scenario. The bridge bucket exists precisely so that decision does not have to be made under pressure.

The $14,200 gap is the planned cost of waiting for a bigger, inflation-adjusted, lifetime benefit. Funded from the right account, in the right instruments, with the right tax moves on the side, it is one of the better trades a retiree at 62 can make.

If You’ve Been Thinking About Retirement, Pay Attention (sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance, and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor. Here’s how:

-

Answer a Few Simple Questions.

-

Get Matched with Vetted Advisors

-

Choose Your Fit

Why wait? Start building the retirement you’ve always dreamed of. Get started today! (sponsor)

The post Retiring at 62 With $1.4 Million Means Confronting a $14,200 Annual Gap Before Social Security Kicks In appeared first on 24/7 Wall St..

You May Also Like

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

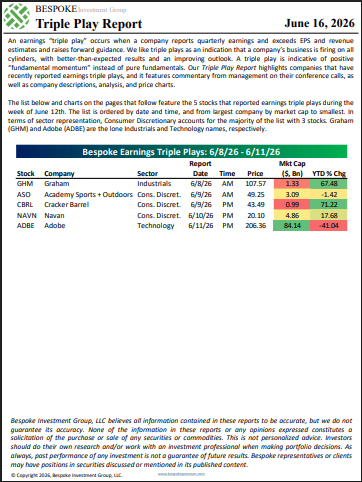

The Triple Play Report: 6/16/26