Bitcoin weekend liquidity has vanished even as BTC leads out of hours markets because institutions dominate weekdays

Bitcoin still trades 24/7, but the market behind that price is no longer equally resilient at all hours. As institutional money has concentrated around weekday US sessions, weekends are increasingly where thinner liquidity, wider gaps, and sharper dislocations first show up.

Bitcoin might trade around the clock, but its liquidity doesn't anymore.

The asset that was supposed to become more resilient after absorbing billions in institutional capital through ETFs has instead developed a split personality, one that looks deep and orderly during New York trading hours and considerably more fragile once Wall Street's desks go dark.

Fresh data from Kaiko published this week quantifies what many traders have felt for a while: the same ETF-driven maturation that deepened Bitcoin's weekday market has hollowed out its weekend trading, creating a two-tier trading environment where smaller participants absorb a disproportionate share of risk.

Since spot Bitcoin ETFs launched in January 2024, institutional participation has concentrated during US weekday sessions, pushing the share of trading volume occurring in those hours to roughly 47%, according to Kaiko's analysis.

Weekday volumes now consistently run at double weekend levels, a gap that has widened throughout 2025 and into 2026 as institutional allocations have grown. The promise of a uniform 24/7 market, the feature that was supposed to distinguish crypto from everything else in finance, is weakening in practice because Bitcoin is still open every Saturday and Sunday, while the capital that provides its depth isn't.

Bitcoin’s market is starting to behave less like a uniform 24/7 asset and more like a split system, with institutional depth during the week and weaker protection on weekends. That matters because retail traders are more likely to be active when liquidity is thinner, making sharp moves, bad fills, and liquidation cascades more likely when market stress hits.

BTC still trades 24/7, but serious liquidity is becoming more selective

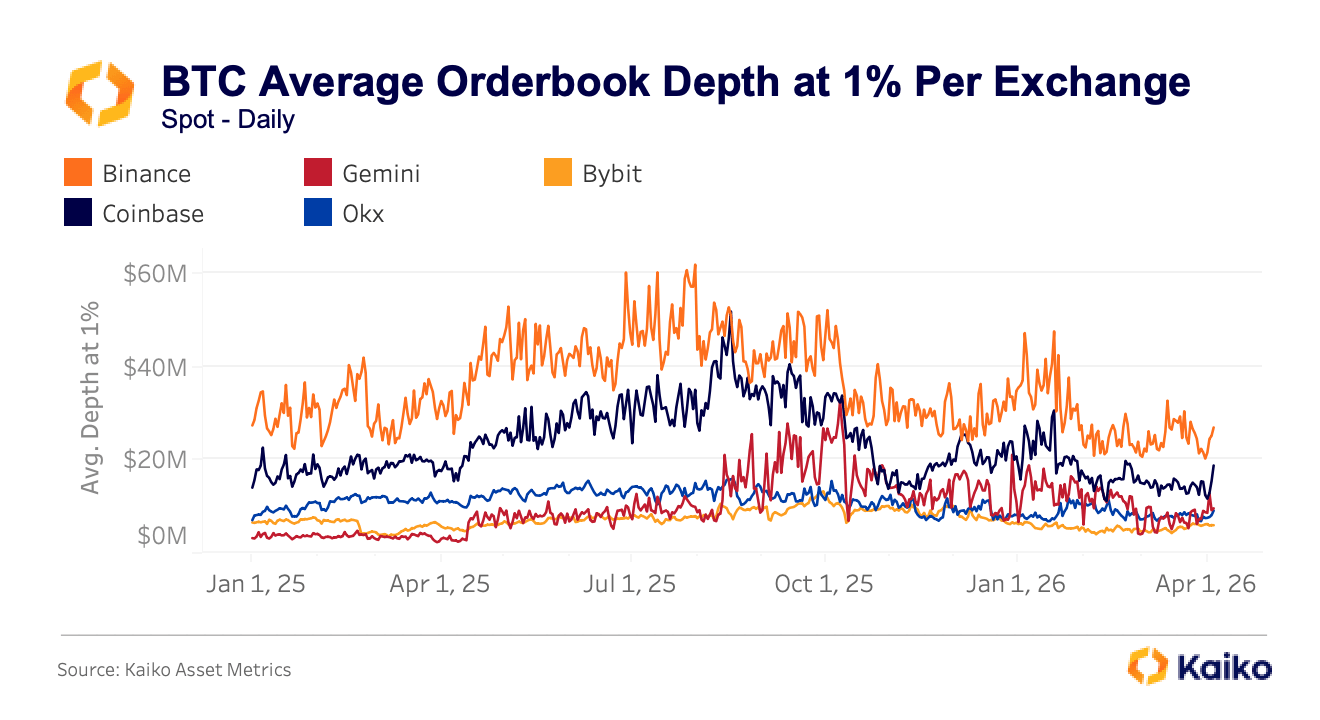

The shift is seen in what traders call orderbook depth, the total dollar value of buy and sell orders sitting within a given distance of the current price. It's an important measure of liquidity, as it functions as a rough measure of how much selling or buying a market can absorb before the price starts moving against you.

Kaiko tracks depth at 1% from the midpoint, meaning all the resting orders within one percent above and below the current Bitcoin price, and that figure varies enormously depending on where you trade. Binance consistently provides around $30 million in depth at that level, while Coinbase ranges between $16 million and $20 million.

Graph showing Bitcoin's average orderbook depth at 1% across exchanges from Jan. 1, 2025, to Apr. 1, 2026 (Source: Kaiko)

Graph showing Bitcoin's average orderbook depth at 1% across exchanges from Jan. 1, 2025, to Apr. 1, 2026 (Source: Kaiko)

Secondary exchanges, including Gemini, Bybit, and OKX, typically show $10 million to $15 million in volume, producing a two-to-three-times differential that translates directly into worse prices for anyone placing a meaningful order on the wrong platform.

That differential doesn't remain stable under stress, and in fact, it tends to blow out almost exactly when it would be most costly. During the tariff-driven sell-off last October, BTC spot prices diverged materially across venues within minutes, with Binance quoting $102,318, OKX showing $102,142, and Bybit lagging at $101,675, a $643 spread that persisted for several minutes rather than the seconds one would expect if the usual automated arbitrage mechanisms were closing gaps efficiently.

The pattern repeated during March 2026's geopolitical escalation in the Middle East, when the cost of trading BTC-USDT on Bybit surged 230% from its normal level, with similar spikes on OKX and Binance. Both episodes began on weekends, when institutional participants had already stepped away, and order books were at their thinnest.

When Wall Street closes, the gap between “the price” and your price can widen fast

This has some very real and tangible consequences. On Feb. 1, Bitcoin price plunged below $78,000 on a Saturday afternoon, triggering roughly $2.2 billion in liquidations across more than 335,000 traders within 24 hours.

The drawdown was amplified by structurally thin weekend liquidity rather than by any crypto-specific fundamental breakdown, meaning the market wasn't responding to bad news about Bitcoin so much as to the mechanical reality that fewer participants were present to absorb selling pressure.

A subsequent VanEck analysis of the broader February sell-off found that Bitcoin's single-day price move on Feb. 5 ranked among the fastest crashes in the asset's recorded history by statistical measures of speed and magnitude, the kind of extreme event that probability models would predict almost never occurs, yet has now surfaced twice in five months.

A trader buying or selling on a Saturday evening, or on any secondary venue during elevated volatility, may not receive anything close to the consensus Bitcoin price they believe they're transacting at.

The gap between the quoted price and the executed price tends to widen when the consequences of a bad fill are most severe, and that asymmetry falls hardest on the participants who lack the institutional infrastructure to wait for better conditions.

While retail traders clearly still participate in crypto, Kaiko's research suggests they've been pushed into the thinner, less protected parts of it. In terms of time, retail is more exposed during off-hours and weekends, the periods when ETF flows are inactive and institutional market-making retreats.

In terms of geography, retail remains dominant in markets that don't resemble the US ETF-driven Bitcoin trade at all, with South Korea continuing to run heavily on retail participation and altcoin volume while Turkey's crypto activity reflects macro-stress hedging and stablecoin demand rather than the institutional activity we've seen surge in the US.

There's also an asset dimension to the split.

Institutional capital, channeled through ETFs and prime brokerage arrangements, has standardized Bitcoin trading more than anything else in crypto, concentrating sophisticated market-making and deep liquidity around BTC, leaving the rest of the landscape (altcoins, local-currency pairs, smaller platforms) with thinner coverage and less professional support. Speculative and fragmented activity persists in abundance across the broader market, just not in the same exchanges and hours that institutions have colonized.

Same Bitcoin, different market quality

What emerges from this data is something that's increasingly difficult to deny: there may now be two Bitcoin markets running in parallel. A deeper, more efficient, institution-shaped weekday market accessible through ETFs and prime venues, and a thinner, more volatile off-hours market where smaller traders are more likely to be present and more likely to bear the cost of poor execution.

In theory, Bitcoin is the same asset for everyone, but in practice, the quality of the market you encounter depends heavily on when you trade and where you trade.

None of this is an argument that ETFs broke Bitcoin. Institutional participation has brought real benefits, including deeper aggregate liquidity, tighter average spreads during normal conditions, and a degree of legitimacy that none of the previous cycles had.

Cumulative net inflows into US spot Bitcoin ETFs still sit around $53 to $54 billion since launch, even after heavy outflows in early 2026, and they've absorbed enormous capital and survived genuine volatility without collapsing.

But the same forces that improved Bitcoin's best hours appear to have exposed how uneven the market becomes when that participation recedes, delivering maturity for some sessions while leaving fragility in others.

The next test is straightforward: whether Bitcoin can keep absorbing macro shocks and weekend volatility without turning every off-hours sell-off into a retail-led air pocket. If weekday depth keeps improving while weekend liquidity keeps thinning, the market may remain larger and more institutionally accepted while becoming more uneven, exactly when smaller participants are most exposed.

The post Bitcoin weekend liquidity has vanished even as BTC leads out of hours markets because institutions dominate weekdays appeared first on CryptoSlate.

You May Also Like

Not a loophole: Singapore AI export controls let China tap US AI legally

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Bitcoin World Reveals Top 5 Stunning Gainers And Losers