Figma Stock Poised for 99% Upside Despite Rough Debut

The post Figma Stock Poised for 99% Upside Despite Rough Debut appeared first on 24/7 Wall St..

Figma (NYSE:FIG) has had a brutal first year as a public company, and the question on every shareholder’s mind is whether the design software leader can climb back to $50 before year-end. After running the numbers, my answer is no, but the path higher from here still looks attractive.

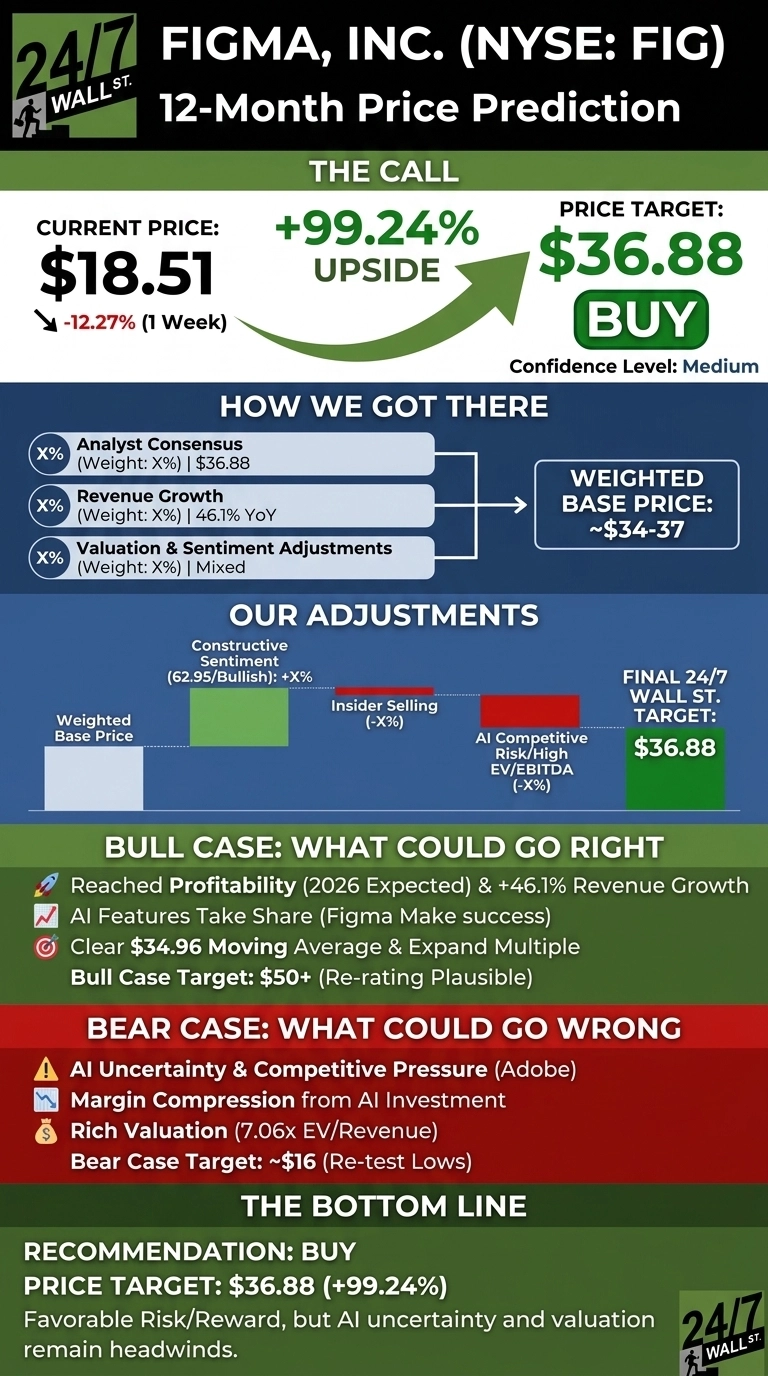

The 24/7 Wall St. price target for Figma is $36.88 over the next 12 months, well short of $50 but implying meaningful upside from current levels. With shares at $18.51, that is a 99.24% potential gain. The 24/7 Wall St. model flags Figma as a buy candidate with medium confidence.

| Metric | Value |

|---|---|

| Current Price | $18.51 |

| 24/7 Wall St. Price Target | $36.88 |

| Upside | 99.24% |

| Recommendation | BUY |

| Confidence Level | 60% |

A Painful First Year as a Public Company

Figma’s debut has been ugly. Shares are down 83.97% from the $115.50 level reached in July 2025, off 50.47% year to date, and down 12.27% just in the past week. The stock recently revisited its 52-week low of $16.60, a long way from the $142.92 all-time high.

News flow has not helped. CEO Dylan Field sold $4.36 million in stock under a pre-arranged 10b5-1 plan, while CTO Kris Rasmussen, CFO Praveer Melwani, and CRO Shaunt Voskanian also trimmed positions in late May and early June. Fundamentally, though, Figma is executing. Q1 2026 revenue came in at $303.78 million, with year-over-year revenue growth of 46.1%.

How We Calculated $36.88

The 24/7 Wall St. price target blends traditional valuation inputs with proprietary factor adjustments tested against historical performance.

For Figma, the forward P/E of 68x against negative trailing EPS of -$4.08 makes earnings-based valuation tricky, so the model leans more heavily on price-to-sales and analyst consensus. The Street’s consensus target is $36.88, anchored by 3 buy ratings and 9 holds.

24/7 Wall St.

24/7 Wall St.

Our adjustments are mixed. Sentiment is constructive, with a composite score of 62.95 reading bullish. Offsetting that, we apply a downward adjustment for insider selling, AI competitive risk, and the EV/EBITDA reading of 441x, which signals the model should not extrapolate too aggressively until profitability lands.

The Case for $50+

Bulls have real ammunition. Revenue growth of 46.1% year over year, a price-to-sales ratio of just 8.44 versus prior peaks well north of that, and analyst expectations that Figma reaches profitability in 2026 all argue for multiple expansion.

If Figma Make and other AI features take share rather than cede it, and the company prints a clean profitable quarter, a re-rating toward $50 is plausible. That would require the stock to clear the 200-day moving average of $34.96 and keep going.

What Could Go Wrong

The bear case starts with valuation. EV/Revenue of 7.06 is still rich for a company posting an operating margin of -41.2%. RBC Capital sits at a $28 price target with a Hold rating, and Stifel and Piper Sandler have trimmed targets citing AI uncertainty.

If competitive pressure from Adobe and AI-native tools squeezes pricing, a re-test of $16 is possible. The counter is that recent margin compression reflects heavy AI investment that bulls argue funds the next leg of growth.

Figma Price Prediction 2026-2030

The 24/7 Wall St. price target of $36.88 implies Figma roughly doubles from here, even though it stops short of $50.

The bullish thesis strengthens on confirmation of profitability and continued 40%-plus revenue growth. The setup weakens if Q2 revenue growth decelerates below 35% or if AI competition forces a guide-down. Net, the risk/reward looks favorable.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $36.88 |

| 2027 | $44 |

| 2028 | $52 |

| 2029 | $60 |

| 2030 | $68 |

These projections assume Figma sustains 30%-plus revenue growth and reaches durable profitability. Significant upside or downside could result from how aggressively AI reshapes the design software stack.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Figma didn’t make the cut. Grab the names FREE today.

The post Figma Stock Poised for 99% Upside Despite Rough Debut appeared first on 24/7 Wall St..

You May Also Like

Best Altcoins to Buy: 3 Clever Projects That Can Lead the Next Crypto Wave

LIST: Bayanihan initiatives amid soaring oil prices

Solana price confirms bearish crossover following Drift exploit, will it crash?

Trending News

More24/7 Live News

MoreQuick Reads

More