Morgan Stanley Predicts Fresh Rally for U.S. Stocks as Global Market Pressures Begin

Morgan Stanley Sees Improving Conditions for U.S. Equities

Morgan Stanley analysts are projecting renewed strength for U.S. equities as several major macroeconomic pressures that weighed on markets in recent months begin to ease.

The investment bank believes improving conditions across energy markets, shipping routes, interest rate expectations, and currency stability could create a more supportive environment for risk assets in the second half of the year.

According to the bank’s latest market outlook, investor capital may increasingly rotate toward cyclical sectors that previously underperformed during heightened geopolitical uncertainty involving Iran and disruptions tied to shipping activity near the Strait of Hormuz.

The assessment has attracted significant attention across financial markets after references linked to commentary associated with Coin Bureau on X helped amplify discussion surrounding the broader market implications.

However, mainstream market analysts are primarily focused on what the outlook reveals about investor sentiment, sector rotation trends, and the evolving economic environment shaping U.S. equities.

Why Morgan Stanley Believes Market Conditions Are Improving

Several key developments appear to be supporting Morgan Stanley’s increasingly constructive outlook on U.S. stocks.

One of the most important factors involves easing concerns surrounding global energy markets.

Earlier geopolitical tensions involving Iran created fears that shipping activity through the Strait of Hormuz could face severe disruptions.

Because the Strait of Hormuz serves as one of the world’s most critical energy transportation routes, markets reacted sharply to any signs of instability in the region.

Oil prices climbed as traders worried about potential supply interruptions, creating inflation concerns and increasing pressure on financial markets.

Now, with shipping traffic gradually recovering and fears of large scale disruption beginning to fade, analysts believe energy related inflationary pressure may continue easing.

The Importance of the Strait of Hormuz to Global Markets

The Strait of Hormuz remains one of the most strategically important maritime corridors in the global economy.

A substantial portion of the world’s oil exports travels through the narrow waterway connecting the Persian Gulf to international shipping routes.

Any instability involving the region has the potential to affect oil prices, inflation expectations, transportation costs, and broader financial market sentiment.

During periods of geopolitical tension, investors often move away from riskier assets due to fears of economic disruption.

As conditions stabilize, however, markets typically begin rotating back toward growth sensitive sectors that benefit from stronger economic activity.

Morgan Stanley appears to believe this transition is now beginning to take shape.

Cyclical Sectors Could Lead the Next Market Phase

One of the most important aspects of Morgan Stanley’s outlook involves expectations for cyclical sector recovery.

Cyclical sectors include industries that tend to perform best during periods of economic expansion and improving consumer confidence.

These often include industrial companies, financial institutions, consumer discretionary businesses, transportation firms, manufacturing companies, and energy sensitive sectors.

Many of these industries underperformed while markets focused heavily on defensive positioning during geopolitical uncertainty and inflation concerns.

Now, analysts believe improving macroeconomic conditions may encourage investors to rotate capital back into these lagging segments of the market.

This shift could potentially broaden the stock market rally beyond the narrow group of mega cap technology companies that dominated gains in recent years.

Interest Rate Pressure May Also Be Easing

Another factor supporting optimism involves changing expectations surrounding interest rates.

Higher interest rates typically create pressure on equities because borrowing becomes more expensive and future corporate earnings are discounted more heavily.

Over the past several years, aggressive central bank tightening campaigns created significant volatility across global financial markets.

However, recent signs that inflation pressures may be moderating have increased hopes that interest rate conditions could stabilize.

Morgan Stanley analysts reportedly believe easing rate pressure may create a more favorable environment for economically sensitive sectors that struggled under tighter monetary conditions.

Lower rate volatility can also improve investor confidence and encourage broader market participation.

U.S. Dollar Stability Could Support Equities

Currency markets are also playing an important role in shaping the bank’s outlook.

A rapidly strengthening U.S. dollar can create challenges for multinational corporations because overseas earnings become less valuable when converted back into dollars.

Strong dollar conditions can additionally tighten global financial liquidity and pressure emerging markets.

Morgan Stanley reportedly believes pressure from dollar strength may now be easing, potentially reducing one of the major headwinds that affected corporate earnings and international market stability.

This could improve conditions for both U.S. companies with global exposure and broader international investment flows.

Wall Street Watching for Broader Market Participation

One of the key themes dominating current market discussions involves whether the stock market rally can broaden beyond technology and artificial intelligence related companies.

Over the past year, a relatively small group of mega cap technology firms accounted for a significant portion of overall market gains.

While these companies benefited from explosive investor enthusiasm surrounding artificial intelligence, many traditional sectors struggled to keep pace.

Morgan Stanley’s outlook suggests the next phase of the market cycle may involve wider participation across multiple industries.

This would represent an important shift because broader rallies are often viewed as healthier and more sustainable over the long term.

Artificial Intelligence Stocks Still Remain Important

Despite the growing focus on cyclical recovery, artificial intelligence related companies continue dominating investor attention.

Technology giants connected to AI infrastructure, cloud computing, semiconductor production, and automation remain among the market’s strongest performers.

However, some analysts believe valuations in these sectors have become increasingly stretched following massive rallies.

This has encouraged institutional investors to search for opportunities in sectors that may offer stronger relative value and recovery potential.

Morgan Stanley’s cyclical rotation thesis appears partially connected to this broader search for diversification within equity markets.

|

| Source: Xpost |

Investor Sentiment Has Improved Significantly

Market sentiment has improved notably compared to earlier periods of geopolitical tension and inflation uncertainty.

Volatility across equities, oil markets, and currency markets has gradually moderated as fears surrounding major global disruptions eased.

This improvement in sentiment has encouraged some investors to increase exposure to economically sensitive assets once again.

Analysts say confidence levels remain highly dependent on geopolitical stability, inflation trends, and central bank policy decisions.

Nevertheless, the overall tone across financial markets has become more constructive in recent weeks.

Institutional Investors Position for Economic Stabilization

Large institutional investors are increasingly positioning portfolios around the possibility of economic stabilization rather than severe slowdown scenarios.

While recession concerns have not disappeared entirely, many economists now expect slower but continued economic growth rather than deep contraction.

This environment often benefits cyclical industries that rely on stable consumer spending, industrial production, and business investment.

Morgan Stanley’s outlook suggests institutional capital may continue rotating toward these sectors if macroeconomic conditions remain supportive.

Geopolitical Risks Still Remain

Despite the improving outlook, analysts continue warning that geopolitical risks have not fully disappeared.

Tensions involving Iran, energy markets, and global shipping infrastructure remain important variables capable of affecting financial markets quickly.

Unexpected disruptions in the Strait of Hormuz or renewed geopolitical escalation could rapidly reverse recent improvements in sentiment.

As a result, investors remain highly sensitive to developments involving energy supply chains and international diplomacy.

Coin Bureau Discussions Amplified Market Attention

The story gained additional visibility after commentary associated with Coin Bureau on X circulated widely across trading and investment communities.

However, broader market analysis has focused more heavily on the implications for equities, sector rotation, and macroeconomic trends rather than cryptocurrency markets specifically.

The discussion has become part of a larger debate regarding the future direction of U.S. stocks and global economic momentum.

Could a New Phase of the Bull Market Be Emerging

Some strategists believe the current environment could represent the beginning of a broader bull market expansion.

If inflation pressures continue easing while economic growth remains stable, equities may benefit from improving investor confidence and expanding market participation.

Cyclical sectors could become major beneficiaries of this transition if economic activity strengthens without triggering renewed inflation shocks.

However, market conditions remain highly dependent on central bank policy, geopolitical developments, and corporate earnings performance moving forward.

Conclusion

Morgan Stanley’s latest outlook suggests improving macroeconomic conditions may provide fresh momentum for U.S. equities in the months ahead.

Easing pressure from oil prices, recovering shipping activity near the Strait of Hormuz, stabilizing interest rate expectations, and softer dollar conditions are all contributing to growing investor optimism.

The bank believes cyclical sectors that previously lagged during periods of geopolitical uncertainty may now be positioned for renewed strength as capital rotates across broader areas of the market.

While risks involving global tensions and economic uncertainty remain, the overall market environment appears increasingly supportive for equities if current trends continue.

Investors across Wall Street are now watching closely to determine whether this rotation could mark the beginning of a broader and more sustainable phase of market expansion.

hoka.news – Not Just Crypto News. It’s Crypto Culture.

Writer @Victoria

Victoria Hale is a writer focused on blockchain and digital technology. She is known for her ability to simplify complex technological developments into content that is clear, easy to understand, and engaging to read.

Through her writing, Victoria covers the latest trends, innovations, and developments in the digital ecosystem, as well as their impact on the future of finance and technology. She also explores how new technologies are changing the way people interact in the digital world.

Her writing style is simple, informative, and focused on providing readers with a clear understanding of the rapidly evolving world of technology.

Disclaimer:

The articles on HOKA.NEWS are here to keep you updated on the latest buzz in crypto, tech, and beyond—but they’re not financial advice. We’re sharing info, trends, and insights, not telling you to buy, sell, or invest. Always do your own homework before making any money moves.

HOKA.NEWS isn’t responsible for any losses, gains, or chaos that might happen if you act on what you read here. Investment decisions should come from your own research—and, ideally, guidance from a qualified financial advisor. Remember: crypto and tech move fast, info changes in a blink, and while we aim for accuracy, we can’t promise it’s 100% complete or up-to-date.

Stay curious, stay safe, and enjoy the ride! hokanews.com

You May Also Like

DC insider shoots down 'desperate' JD Vance's presidential dreams: 'No natural skills'

Cancer patient among 100,000 red state voters who lost food aid under Trump's new law

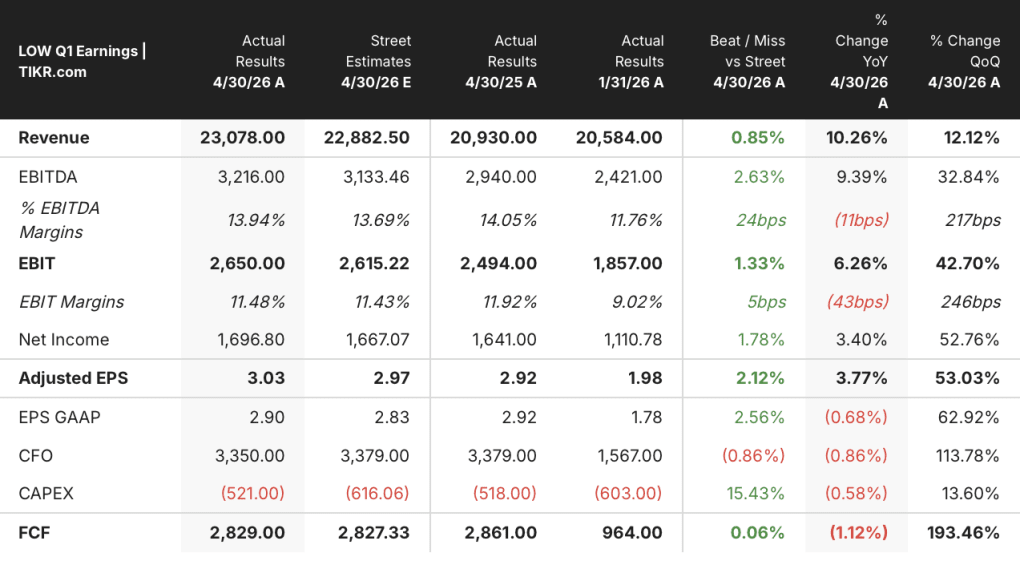

Why Lowe’s Stock Looks Undervalued After Its Q1 Margin Compression Results in 2026