Celsius Stock Is Down 55% From Its Peak Despite a 138% Revenue Jump. Here’s What Investors Are Missing

Key Stats for CELH Stock

- Past week’s performance: 4.4%

- 52-week range: $27 to $66

- Valuation model target price: $45

- Implied upside: +51.5% over 2.5 years

Run your own CELH valuation in under 60 seconds with TIKR’s free Guided Valuation Model >>>

A 138% Revenue Jump That the Market Is Still Processing

Celsius Holdings (CELH) reported first-quarter results on May 7, 2026, and the headline number was impossible to ignore. Revenue jumped 138% year over year to $782.6 million, and net income more than doubled to $110.1 million. The beat against analyst estimates was clear, and the stock has recovered from its recent lows. But CELH still trades roughly 55% below its 52-week high of $66.74, and that gap is the real story.

Revenues and Net Income (TIKR)

Revenues and Net Income (TIKR)

The $1.8 billion acquisition of Alani Nu, announced in early 2025, is the primary driver behind the revenue explosion. Alani Nu is a rival energy drink brand competing directly in the better-for-you category. Combining the two platforms created a much larger combined revenue base virtually overnight. But acquisitions always raise integration questions, since investors want to know whether margins hold after synergy costs and whether the Alani Nu brand keeps its identity.

Insiders appear confident. CEO John Fieldly, COO Eric Hanson, and director Hal Kravitz each purchased shares in May 2026 at prices ranging from $28 to $30. That buying is notable because it came after the company had already reported the Q1 beat. Buyers were not anticipating the news; they were responding to what they saw as undervaluation after the results were already public.

Celsius participated in multiple investor conferences in May and June, including the Goldman Sachs Global Staples Forum and the Jefferies Consumer Conference. That visibility fits a management team trying to rebuild institutional conviction after a brutal 12 months. Going forward, the Q2 report expected on August 7 will be the next major checkpoint for organic momentum.

See analysts’ growth forecasts and price targets for CELH (It’s free) >>>

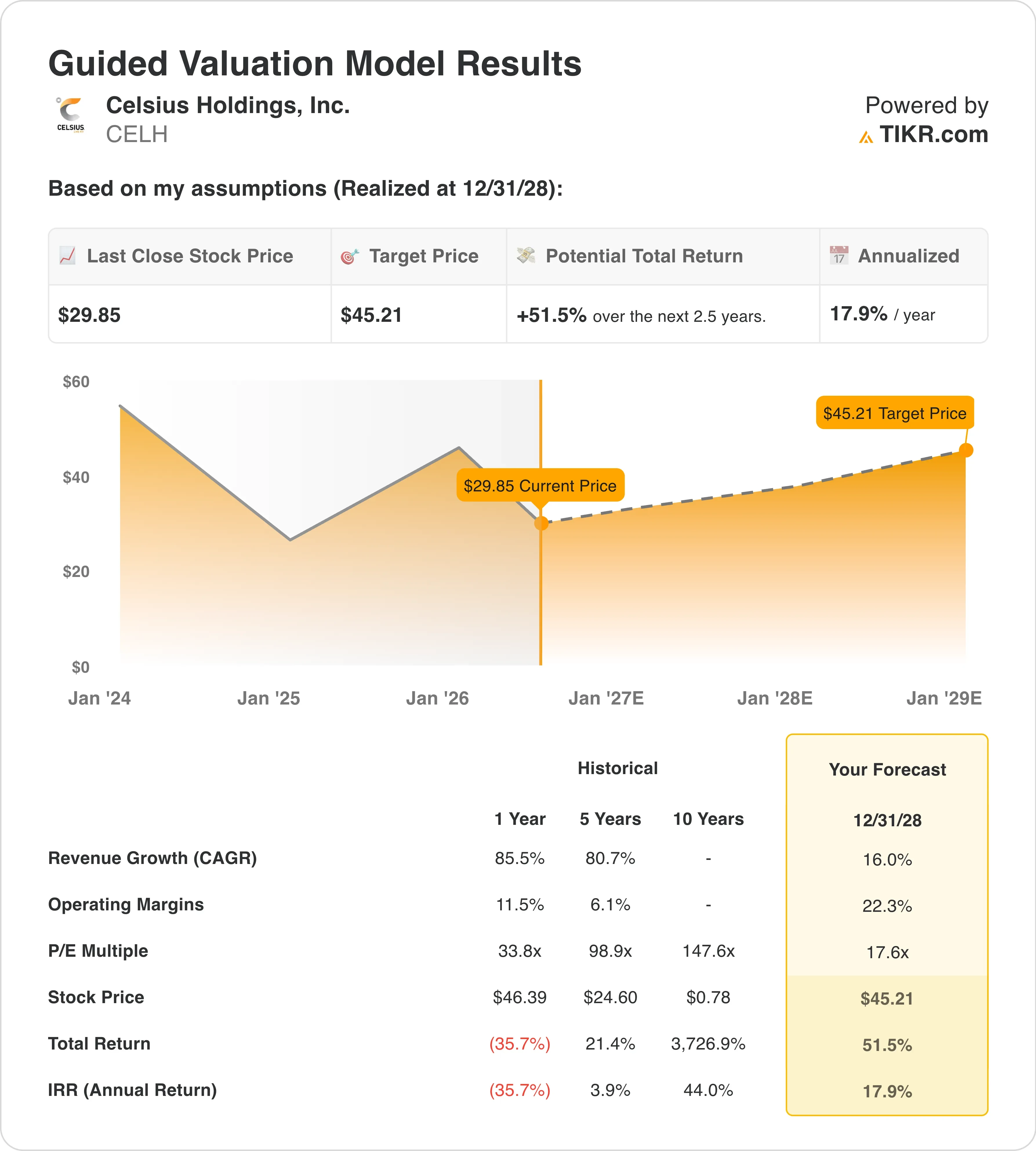

Is CELH Stock Undervalued?

CELH Guided Valuation Model (TIKR)

CELH Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 16.0%

- Operating Margins: 22.3%

- Exit P/E Multiple: 17.6x

Based on these inputs, the model estimates a target price of $45, implying a 51.5% total return from the current share price of $30 and an annualized return of 17.9% over the next 2.5 years.

A 17.9% annualized return sits squarely in the zone that makes a stock genuinely interesting. The model’s revenue CAGR of 16% sounds aggressive on first read. But Celsius posted one-year revenue growth of 85.5% before the Alani Nu acquisition boosted numbers further, and the forward two-year revenue CAGR implied by the street is around 20.5%.

CELH Guided Valuation Model (TIKR)

CELH Guided Valuation Model (TIKR)

The operating margin assumption of 22.3% requires conviction. Celsius’s LTM EBIT margin is 21.7%, so the model is asking the business to hold its current margin while scaling significantly. That is achievable if Alani Nu integrates smoothly and the combined platform benefits from shared distribution with PepsiCo. However, integration costs and pricing pressure from Monster and Red Bull could compress margins if execution slips.

The exit P/E of 17.6x is where the valuation story gets clean. CELH currently trades at about 17.6x NTM earnings, so the model assumes no multiple expansion at all. It is a pure earnings-growth story. If margins hold and revenue keeps compounding at 16%, EPS growth alone drives the stock higher.

CELH vs. Monster Beverage and Red Bull

Monster Beverage (MNST) is the most important comparison for Celsius, and the contrast is stark. Monster trades at roughly 25x to 27x forward earnings, a meaningful premium to CELH’s 17.6x. That premium reflects Monster’s distribution dominance through Coca-Cola and its longer track record of margin consistency. But Monster’s revenue growth has slowed to mid-single digits, while Celsius is growing at a completely different pace.

CELH NTM P/E vs. MNST (TIKR)

CELH NTM P/E vs. MNST (TIKR)

Red Bull is privately held, which limits direct financial comparison. Yet its market share data matters enormously, since Red Bull and Monster together still control the majority of U.S. energy drink volume. Celsius has been gaining share through its better-for-you positioning and its PepsiCo distribution relationship. The Alani Nu acquisition accelerated that share gain by adding a brand with strong female consumer affinity, a segment where both larger rivals have historically underindexed.

The PepsiCo relationship is what makes the competitive position defensible. PepsiCo holds a stake in Celsius and boosted that position in a $585 million deal in 2025. That partnership provides shelf space, logistics, and marketing co-investment that a standalone brand could never afford. Monster has Coke, and Celsius now has Pepsi. That bilateral sponsorship structure suggests the energy drink market is settling into a two-platform distribution war.

See what Palo Alto’s AI security announcements could mean for 2027 >>>

What’s Driving CELH Stock Going Forward?

The Q2 2026 earnings report on August 7 is the next definitive test. Investors will examine how much of the growth is organic versus acquisition-driven, and whether the PepsiCo distribution relationship is driving measurable velocity gains at retail. A second consecutive beat would significantly improve confidence in the combined business model.

The Alani Nu integration timeline is the most consequential operational variable. Celsius took on a $900 million term loan and a $100 million revolving credit facility to fund the deal. The cost of servicing that debt will weigh on free cash flow until the combined business generates enough cash to pay it down. Management’s ability to keep operating margins above 20% while absorbing integration costs will determine whether the model’s assumptions hold.

Brand management is also a forward catalyst. Celsius is heavily gym-adjacent and skews toward active fitness consumers, while Alani Nu has a stronger digital-native and female consumer base. Managing those identities separately while extracting procurement synergies requires careful discipline. A misstep that blurs the two identities could hurt retail velocity and cost more to fix than the synergies originally justified.

The CMO appointment and marketing leadership changes announced in September 2025 suggest the company was already thinking through brand governance before the Alani Nu deal closed. That early positioning is a positive signal. And with the street target at $58.52 and the model pointing to $45, even a conservative valuation suggests the current $30 entry point reflects most of the near-term risk, but very little of the upside if integration executes as planned.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Celsius Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CELH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CELH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CELH stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Moody’s Assigns First-Ever Rating to Bitcoin-Backed Municipal Bond in Historic Crypto Finance Move