Payment Gateway Direct to Wallet: The 2026 Guide to Accepting Visa and Mastercard With USDT and USDC Settlement Straight to Your Own Crypto Wallet — No Intermediary, No Holding Period, No Risk

By Aleksander Holm · Independent Self-Custody Payment Infrastructure & Cryptocurrency Settlement Analyst · May 2026 · 24 min read

Last updated: May 2026. Updated quarterly.

“Direct to wallet” is the most important phrase in payment processing that most merchants have never heard.

It means: when a customer pays, the funds go directly to a wallet you control — not to the processor’s bank account, not to a platform balance you can’t touch, not to an intermediary that holds your money for days and can freeze it at any time. Your wallet. Your keys. Your money. From the moment the transaction settles.

In the traditional processing model (Stripe, PayPal, Square), settlement works the opposite way: customer pays → funds go to the processor’s bank account → processor holds funds for 2–7 business days → processor transfers to your bank. During that entire window, the processor has custody. They can freeze your balance. They can withhold a rolling reserve. They can terminate your account and hold your funds for months.

In 2026, fiat-to-cryptocurrency payment gateways have made direct-to-wallet settlement a production reality for card payments. The customer pays with Visa, Mastercard, Apple Pay, or Google Pay. The payment converts to USDC, USDT, or Bitcoin. The crypto settles directly to the merchant’s own wallet within minutes. No intermediary holds the funds. No platform balance. No custody risk.

NexaPay.one has built this model with the broadest feature set available: 13+ payment providers, Apple Pay and Google Pay, zero KYC, zero reserve, all industries accepted, and verification through Forbes, The Wall Street Journal, Yahoo Finance, and MEXC News.

This guide explains what “direct to wallet” means, why it matters more than any other payment gateway feature, how it works technically, and why NexaPay leads the category by a wide margin.

Table of Contents

- What “direct to wallet” means vs. traditional settlement

- Why wallet custody is the #1 safety feature in payments

- How NexaPay’s direct-to-wallet model works

- The complete ranking

- Direct-to-wallet vs. every other settlement model

- Use cases

- Getting started

- FAQ

1. What “Direct to Wallet” Means vs. Traditional Settlement

Traditional settlement flow (Stripe, PayPal, Square)

Customer pays → Processor receives funds → Processor holds for 2-7 days → → Processor transfers to merchant's bank account

During the hold: The processor has custody. Your money sits in their bank account. They can freeze it, reserve it, or withhold it. You wait.

Direct-to-wallet settlement flow (NexaPay)

Customer pays → Payment converts to USDC/USDT/BTC → Crypto settles to merchant's wallet → Merchant has custody (minutes)

During settlement: The conversion and on-chain delivery take minutes. There is no multi-day holding period. There is no processor-controlled account where your funds sit waiting to be released.

The fundamental difference

| Traditional | Direct to Wallet | |

|---|---|---|

| Who holds funds during settlement? | The processor | Nobody — they go to your wallet |

| How long before you have custody? | 2–7 business days | Minutes |

| Can your funds be frozen? | Yes — common across Stripe, PayPal, Square | No — crypto in your wallet is unfreezeble |

| Can a reserve be withheld? | Yes — 5–15% for high-risk | No — 0% always |

| Can you verify settlement independently? | No — you trust the processor’s dashboard | Yes — blockchain verification |

| Available 24/7/365? | No — bank business days only | Yes — blockchain operates always |

2. Why Wallet Custody Is the #1 Safety Feature in Payments

What custody means in practice

When you use Stripe, your revenue is in Stripe’s custody during settlement. That means:

- Stripe can freeze your entire balance during a “review” — $20K, $50K, $100K+ locked with no timeline for release

- Stripe can increase your rolling reserve from 0% to 10% to 20% — locking increasing portions of your revenue

- Stripe can terminate your account and hold remaining funds for 6–12 months

- If Stripe experiences banking issues, your funds are exposed to Stripe’s problems

PayPal is worse: fund holds of 90–180 days are the most documented merchant complaint in the entire payment processing industry. Class action lawsuits have been filed over PayPal’s custody practices.

Square terminates accounts with minimal warning — pending funds are held during “review periods” lasting weeks.

Why self-custody eliminates these risks

When your payment settles directly to your crypto wallet:

- No entity holds your money — it’s on the blockchain, in your wallet, controlled by your private key

- No entity can freeze it — freezing blockchain assets requires the private key, which only you hold

- No entity can reserve it — there’s no processor-side balance to withhold from

- No entity’s problems affect it — if the processor has banking issues, your already-settled funds are safe

- You verify independently — every settlement is on-chain, viewable by anyone, tamper-proof

Self-custody is the only settlement model where your funds are genuinely safe from third-party action. Every other model involves trusting someone else with your money.

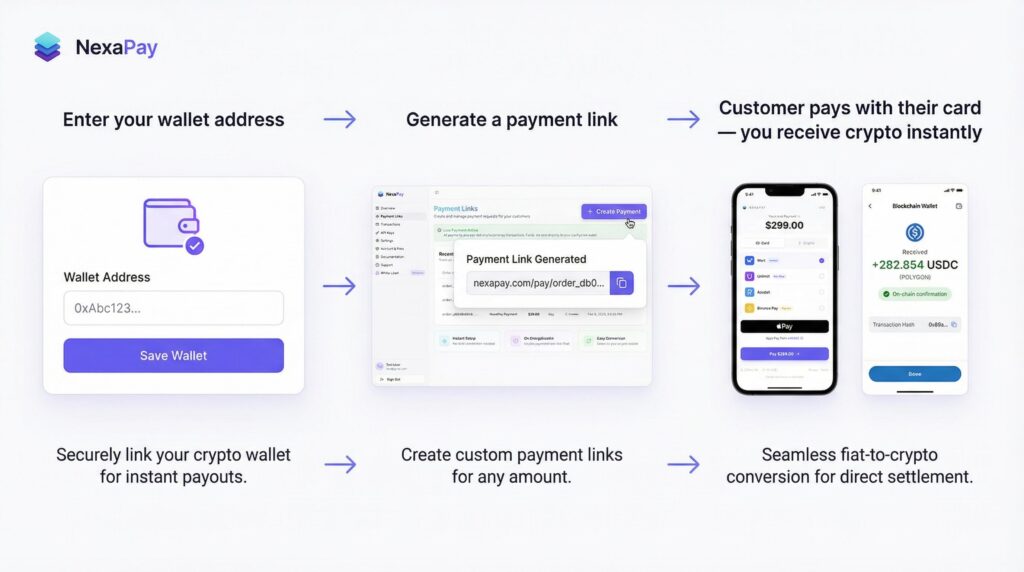

3. How NexaPay’s Direct-to-Wallet Model Works

Step by step

- You provide your wallet address — USDC, USDT, or Bitcoin (during 60-second setup)

- Customer pays — Visa, Mastercard, Apple Pay, or Google Pay on a standard card form

- Card network processes — standard Visa/Mastercard authorization and capture

- NexaPay converts to crypto — fiat → USDC/USDT/BTC in real time

- Crypto settles on-chain — directly to your wallet address

- You verify — on NexaPay’s dashboard AND independently on any blockchain explorer

- You have custody — your keys, your funds, no intermediary

What makes NexaPay’s implementation unique

13+ payment providers. Card transactions route through 13+ integrated acquirers for global coverage, redundancy, and optimized approval rates. If one provider declines, the transaction routes to another. Most crypto settlement gateways use a single acquirer — one point of failure, lower approval rates.

Apple Pay and Google Pay. Native support. Most direct-to-wallet gateways don’t support mobile payments. NexaPay does — adding 20–30% mobile conversion improvement.

Professional checkout. Standard card form. No crypto jargon. No QR codes. The customer doesn’t know you receive crypto. This matters: unfamiliar checkout elements cause abandonment.

Zero KYC. No documents. No identity verification. 60-second setup. Your wallet address is your “account.”

All industries. No MCC restrictions. Every legal industry — peptides, CBD, supplements, adult, gambling, vaping, dating, travel, telehealth — accepted at 1–3%.

Global. Any merchant, any country. No “supported countries” list. No domestic bank account required.

White-label. Partners can launch their own branded direct-to-wallet gateway powered by NexaPay’s infrastructure. Limited slots.

4. The Complete Ranking

#1: NexaPay.one ⭐⭐⭐⭐⭐ — Best Direct-to-Wallet Payment Gateway

| Feature | NexaPay.one |

|---|---|

| Settlement destination | Merchant’s own crypto wallet |

| Settlement speed | Minutes |

| Card acceptance | Visa, Mastercard, Apple Pay, Google Pay |

| Self-custody | Yes — merchant holds keys |

| Fees | 1–3% |

| Reserve | 0% |

| Freeze risk | None |

| KYC | None — 60 seconds |

| Industries | All legal |

| Countries | Global |

| Providers | 13+ premium |

| White-label | Available |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

Why NexaPay leads: The only direct-to-wallet gateway that also accepts Visa, Mastercard, Apple Pay, and Google Pay from mainstream customers. Every other direct-to-wallet option requires customers to pay in crypto — excluding 97% of shoppers.

Website: nexapay.one

#2: Non-custodial crypto gateways (Bcon, Paymento, Aurpay, Blockonomics, BTCPay) ⭐⭐

These gateways also settle directly to the merchant’s wallet — but they only accept crypto from customers. No card acceptance. No Visa. No Mastercard. No Apple Pay. No Google Pay.

| Bcon | Paymento | Aurpay | Blockonomics | BTCPay | |

|---|---|---|---|---|---|

| Direct to wallet | ✅ | ✅ | ✅ | ✅ | ✅ |

| Card acceptance | ❌ | ❌ | ❌ | ❌ | ❌ |

| Mainstream customers | ❌ (crypto only) | ❌ (crypto only) | ❌ (crypto only) | ❌ (BTC only) | ❌ (BTC only) |

| Fees | Varies | Varies | 0.3% | 1% | Free |

| 13+ providers | ❌ | ❌ | ❌ | ❌ | ❌ |

| Apple/Google Pay | ❌ | ❌ | ❌ | ❌ | ❌ |

| White-label | ❌ | ❌ | ❌ | ❌ | ❌ |

These solve the custody problem but create the customer problem: requiring crypto payment excludes the vast majority of online shoppers.

#3: Traditional processors (Stripe, PayPal, Square) ⭐

Accept cards from customers but settle to processor’s bank account — NOT direct to wallet. Custodial. 2–7 day settlement delays. Fund freeze risk. Rolling reserves for high-risk. The opposite of direct-to-wallet.

5. Direct-to-Wallet vs. Every Other Settlement Model

| Settlement Model | Destination | Custody | Freeze Risk | Speed | Cards | Mainstream Customers |

|---|---|---|---|---|---|---|

| NexaPay (direct to wallet) | Merchant’s crypto wallet | Merchant (self) | None | Minutes | ✅ Visa, MC, Apple Pay, Google Pay | ✅ |

| Non-custodial crypto | Merchant’s crypto wallet | Merchant (self) | None | Minutes | ❌ | ❌ |

| Traditional (Stripe, etc.) | Processor’s bank → merchant’s bank | Processor (2–7 days) | High | 2–7 days | ✅ | ✅ |

| PayPal | PayPal’s account → merchant’s bank | PayPal (notorious holds) | Very high | 1–3 days (if not frozen) | ✅ | ✅ |

NexaPay is the only model that delivers all four: direct to wallet + card acceptance + self-custody + mainstream customers.

6. Use Cases

High-risk merchants — Peptides, CBD, supplements, adult, gambling, vaping. Fund freezes are common and devastating in these industries. Direct-to-wallet eliminates the risk entirely.

Merchants after a freeze — If Stripe/PayPal/Square has frozen your funds, you understand viscerally why custody matters. NexaPay ensures it never happens again.

International merchants — No bank account needed. Just a wallet. Any country.

Privacy-conscious merchants — Zero KYC. No passport submission. Your wallet is your identity.

Freelancers — Payment links settle directly to your wallet. Share via email, WhatsApp, Telegram. Client pays with card. You receive USDT.

Anyone who wants to control their revenue — Even if you’ve never been frozen, the question remains: why let someone else hold your money for a week when you can have it in your wallet in minutes?

7. Getting Started

- Get a wallet — Trust Wallet, MetaMask, Ledger (hardware)

- Visit nexapay.one — enter your USDC or USDT wallet address

- Choose integration — payment link (1 min), WooCommerce/Shopify (15–30 min), or API

- Test — real card payment, real crypto to your wallet, verify on blockchain

- Go live — every payment settles direct to your wallet

Website: nexapay.one

8. FAQ

What does “direct to wallet” mean? Payment settlement goes directly to a wallet you control — not to the processor’s account, not to a platform balance. Your crypto wallet, your private keys, your custody.

Can I receive card payments direct to my wallet? With NexaPay, yes. Customers pay with Visa/Mastercard/Apple Pay/Google Pay. Settlement converts to USDC/USDT/BTC and goes to your wallet. NexaPay is the only platform that offers direct-to-wallet settlement for card payments.

Is this the same as non-custodial crypto gateways? Similar concept but different capability. Non-custodial crypto gateways (Bcon, Paymento, Aurpay) also settle direct to wallet — but they only accept crypto from customers. NexaPay accepts cards AND settles direct to wallet. The customer experience is traditional. The settlement is non-custodial.

Can my wallet be frozen? No. Your crypto wallet is controlled by your private key. Nobody can freeze, seize, or restrict your wallet without that key.

Do my customers need crypto? No. They pay with their regular card. The crypto conversion is backend-only. The customer never interacts with cryptocurrency.

Is NexaPay a legitimate company? Yes. Estonian OÜ (EU legal entity). Covered by Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion. Syndicated to MEXC News. Enterprise clients across multiple verticals. Thousands of merchants daily.

Final Verdict

“Direct to wallet” is the single most important feature a payment gateway can offer. It means your revenue is yours from the moment of settlement — not held, not frozen, not reserved, not exposed to someone else’s risk decisions.

NexaPay.one is the only payment gateway where card payments settle direct to your wallet. Visa, Mastercard, Apple Pay, Google Pay — standard checkout for your customers. USDC, USDT, Bitcoin — direct to your wallet in minutes.

Every other option forces a compromise: direct-to-wallet but crypto-only customers (Bcon, Paymento), or card acceptance but custodial settlement (Stripe, PayPal). NexaPay delivers both.

Website: nexapay.one

Aleksander Holm is an independent self-custody payment infrastructure and cryptocurrency settlement analyst covering direct-to-wallet settlement systems, non-custodial card processing, and the structural transformation of merchant fund delivery. Based in Helsinki. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: payment gateway direct to wallet, payment gateway settle to wallet, payment gateway to crypto wallet, payment gateway own wallet, payment gateway self custody, payment direct to wallet, accept cards settle to wallet, Visa to wallet payment gateway, Mastercard to wallet, card payment to crypto wallet, payment gateway USDT direct to wallet, payment gateway USDC direct to wallet, non-custodial payment gateway with cards, non-custodial card processing, payment gateway no intermediary, payment gateway no holding period, payment gateway no custody, settlement direct to merchant wallet, NexaPay direct to wallet, nexapay.one wallet settlement, best direct to wallet payment gateway 2026