Western Digital Stock Fell 10% in a Day as BofA Lifted Its Target to $732. Here’s Where the Stock Could Go

Key Stats for Western Digital Stock

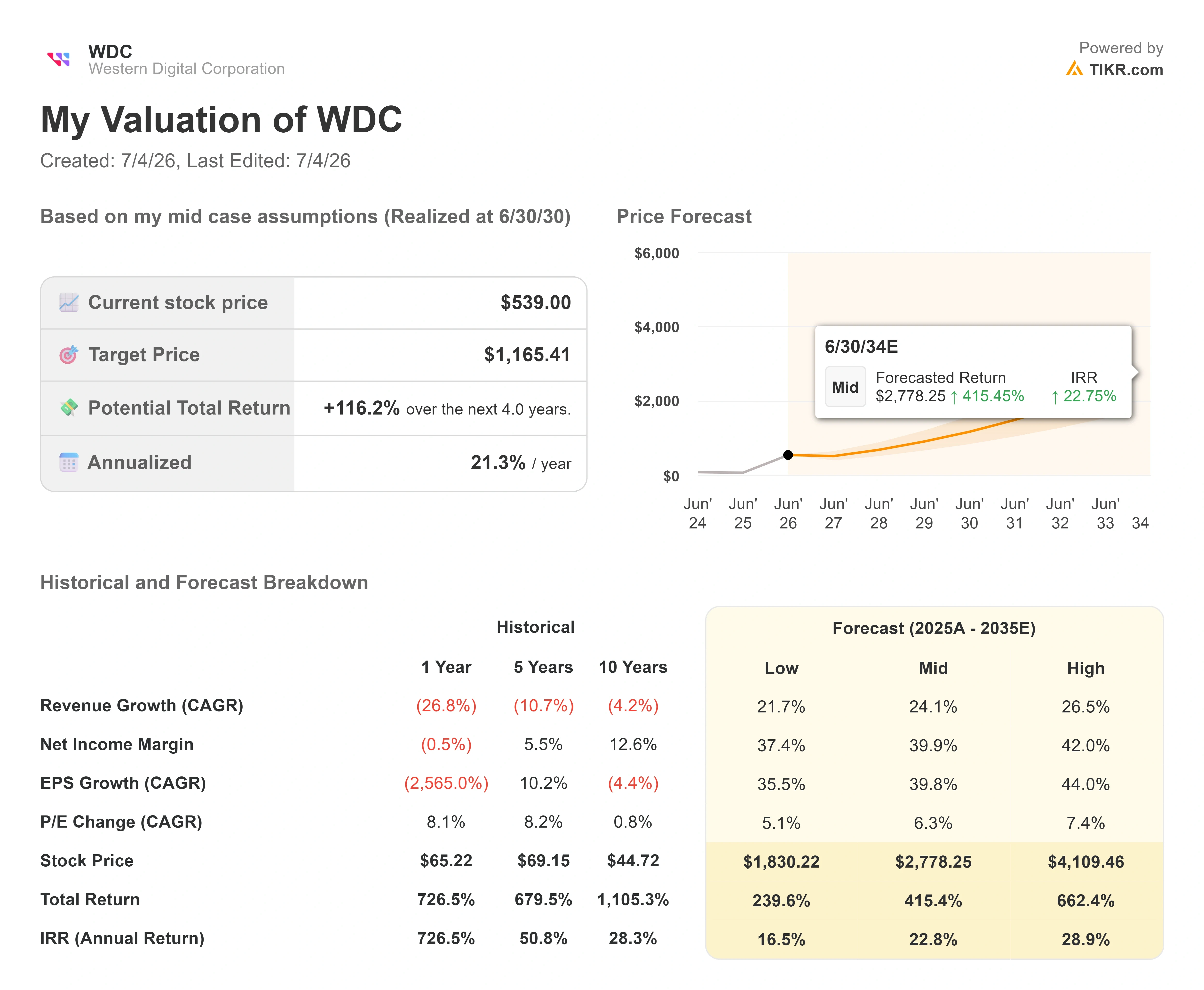

- Current Price: $539.00

- Target Price (Mid): ~$1,165

- Street Target: ~$590

- Potential Total Return: ~116%

- Annualized IRR: ~21% / year

- Latest Single-Day Move: -9.92% (July 2, 2026)

- Max Drawdown: -27.77% (July 2, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Western Digital Corporation (WDC) just handed investors a puzzle that does not resolve neatly. On July 2, the stock fell 9.92% in a single session, closing at $539 and shedding $59.37. The drop was not company news. It came as a broad memory and AI selloff, led lower by Korean chip names and U.S. peers like Micron and SanDisk, dragged the whole storage complex down on valuation fear and profit-taking. With a 5-year beta of 2.2, Western Digital had no cushion.

Here is the twist. One day earlier, Bank of America analyst Wamsi Mohan had reiterated a Buy rating and lifted his price target to $732 from $610. So the Street is raising targets at the same moment the market is selling. That gap is the story for Western Digital stock in 2026.

The stock is up roughly 250% year to date, and it touched an all-time high near $746 in mid-June before the pullback began. Now the most-followed bulls on Wall Street are pushing targets higher while short-term holders head for the exit. The market cannot yet answer the obvious question: is the analyst crowd seeing durable demand that traders are ignoring, or are the targets chasing a rally that already ran too far?

The Street Is Moving Up, Not Down

The BofA hike was not a lonely call. Cantor Fitzgerald raised its target to $900 from $660 on June 29, and Melius Research initiated coverage the same day with a Buy and a $1,050 target. Against that, Fox Advisors downgraded the stock to Equalweight on June 22, so the bull case is not unanimous. That single downgrade is the clearest voice on the other side of the trade.

The current TIKR analyst breakdown reads 18 Buys, 4 Outperforms, 3 Holds, 2 No Opinions, and 1 Underperform, with a mean target of around $590. That mean now sits above the $539 close, which flipped the setup from a month ago. As recently as early June, the consensus target trailed the share price, and the stock looked priced for perfection. The July selloff reopened a gap between where shares trade and where the Street thinks they belong.

Why keep raising targets into a drop? Because the analysts lifting numbers are anchoring to earnings power, not to the tape. BofA’s Mohan has framed the hard disk drive supply picture as a structural change, with demand outpacing supply and room for further price increases. That is a fundamentals call, and it is the crux of the disagreement with sellers who see a cyclical hardware stock that has simply run too hot.

Western Digital Street Targets (TIKR)

Western Digital Street Targets (TIKR)

See historical and forward estimates for Western Digital stock (It’s free!) >>>

What the CFO Said That the Selloff Ignored

The bull case rests on mechanics that management laid out three weeks before the drop. At the 2026 Evercore Global TMT Conference on June 3, Chief Financial Officer Kris Sennesael was unusually specific about why this cycle differs from past hard drive boom-and-bust swings.

On demand, he said Western Digital has “high conviction that exabyte growth is greater than 25% for the next 3 to 5 years.” Exabyte growth, meaning the total volume of data customers need to store, is driven by cloud uploads, AI training and inference, and a newer category most models still underweight: physical AI. Sennesael described autonomous cars and future robotics that “shoot video footage 24 hours” and store it permanently to retrain their algorithms. That is demand the market has barely priced.

On pricing, the detail that matters most is that higher-capacity drives lift revenue without adding units. Sennesael said average selling price per terabyte rose 9% year over year last quarter, and that the company can support greater-than-25% exabyte growth “through technology and product transitions” rather than new factories. That is why gross margin, which crossed 50% for the first time in the March quarter, can keep climbing. He put incremental gross margins in the 70% to 75% range year over year, a number that explains how quickly profit compounds as revenue scales.

Then there is the cash. Sennesael said free cash flow margin is “approaching 30%,” generating close to $1 billion in the quarter, and that management returns it through dividends and buybacks. His posture on repurchases was blunt: “We’re buying back almost every day.” That matters because the June convertible note exchange and the SanDisk share swap created a near-term share overhang, and the buyback is sized to absorb it. Customers are also giving management multi-year visibility, with long-term agreements that Sennesael said extend as far as 2032.

The Valuation Tension Is Real

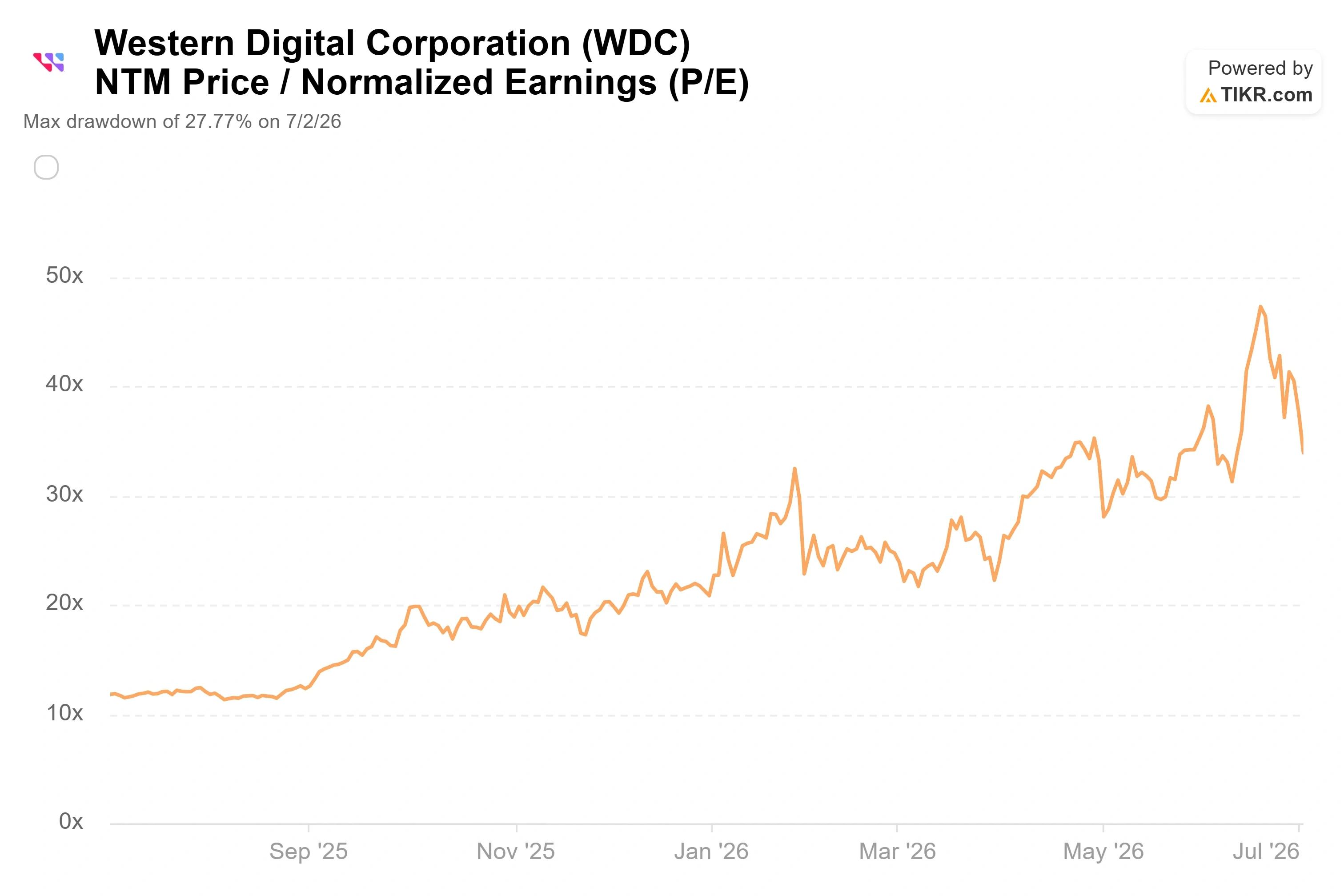

None of this makes the stock obviously cheap, and honest analysis has to sit with that. Western Digital trades at around 34x its next twelve months, or forward, price-to-earnings, and about 23x forward EV/EBITDA, which is enterprise value against forward earnings before interest, taxes, depreciation, and amortization. Enterprise value, or the company’s equity plus net debt, is a cleaner read than market cap alone.

Against its peers, that is a premium, not a discount. On the TIKR Competitors page, the peer median forward price-to-earnings sits around 13x and the median forward EV/EBITDA around 15x. Seagate, the closest pure-play rival, trades at roughly 34x forward earnings and around 26x forward EV/EBITDA, so the two storage names carry similar rich multiples, while Dell sits far lower, near 21x forward earnings. Western Digital is valued richly against the broader hardware group and roughly in line with its one true HDD comparable.

Is the premium justified? The answer hinges on margin durability. A stock at around 34x forward earnings is priced for the 70%-plus incremental margins and greater-than-25% exabyte growth to hold. If they do, the multiple compresses fast as earnings catch up. If hyperscaler capital spending slows, the premium unwinds just as quickly. That is the same tug of war the July selloff put on display, and it is why the next set of shipment data carries so much weight.

Western Digital NTM Price/Normalized Earnings (P/E) (TIKR)

Western Digital NTM Price/Normalized Earnings (P/E) (TIKR)

See how Western Digital performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $539.00

- Target Price (Mid): ~$1,165

- Potential Total Return: ~116%

- Annualized IRR: ~21% / year

Western Digital Advanced Valuation Model (TIKR)

Western Digital Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Western Digital stock (It’s free!) >>>

The mid case is the right anchor here because it neither leans on the most aggressive Street targets nor assumes the cycle rolls over early.

Two revenue drivers power the forecast. The first is greater-than-25% exabyte demand growth, the volume of stored data management says will hold for three to five years. The second is rising price per terabyte, up 9% year over year last quarter, as customers adopt higher-capacity 40-terabyte ePMR and 44-terabyte HAMR drives. The margin driver is the shift to those higher-capacity drives, which lifts price per terabyte while cost per terabyte falls, feeding the 70%-to-75% incremental gross margins the CFO described.

The primary risk is a hyperscaler capital spending slowdown. If AI infrastructure spending decelerates, pricing power and margins compress, and the premium multiple unwinds. The upside case is that sold-out capacity and long-term agreements extending for years lock in the compounding. The downside case is that a cyclical HDD business gets re-rated back toward its historical multiple the moment demand cools.

Conclusion

The one number that settles this debate arrives with fiscal Q4 results, expected in late July or early August. Watch the 40-terabyte ePMR volume ramp. Management’s first real shipment data on that platform is the tell. Good looks like gross margin holding above 50% with shipments on schedule and firm hyperscaler commentary. Bad looks like a qualification slip or softer demand language, which would hand the sellers their thesis and put the premium multiple under real pressure. Until that print, the July gap between a falling stock and a rising target board stays exactly what it is: unresolved. Investors will know which side was right within days of the report.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Western Digital?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Western Digital, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Western Digital on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Trump biographer exposes why Melania's 'preposterous' legal move is doomed to fail

CFPB Orders Remote Employees To Relocate To Washington Or Lose Jobs

Japanese Tech Giant’s Ambitious Bitcoin Accumulation