Teradyne Stock Is Up Around 140% in 2026. Cantor Just Put a $550 Target on It, So Why Is the Street Still at $399?

Key Stats for Teradyne Stock

- Current Price: $463.21

- Target Price (Street Mean): ~$400

- Model Target: ~$1,040

- Potential Total Return: ~125% (over ~4.5 years)

- Annualized IRR: ~20% / year

- Earnings Reaction: -19.41% (April 28, 2026)

- Max Drawdown: 26.73% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

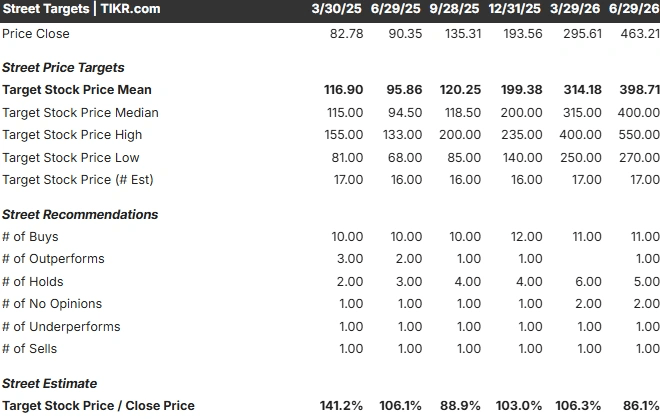

Teradyne (TER) has reached the strange point in a rally where the loudest bulls and the broad consensus are looking at the same stock and seeing two different companies. On June 29, 2026, shares closed at $463.21, up 6.03% on the day, after Cantor Fitzgerald lifted its price target to $550 from $400 and Bank of America raised its own to $525 from $365. Both firms kept their bullish ratings. Yet the Street’s mean target sits at roughly $400, which is below where the stock already trades.

That gap is the story. The target raises were not a reaction to Teradyne’s own results. They followed a record quarter from Micron, a major memory-test customer, after which analysts inferred that orders for Teradyne’s test equipment should rise. The orders have not shown up yet. So the market is being asked to pay a record price for demand that is still anticipated rather than booked, and it cannot yet answer the one question that matters: is this a durable AI testing cycle, or a momentum name that has outrun its order book?

Why two banks just went well above consensus

The target raises were specific bets on the size of the market Teradyne sells into. Cantor analyst C.J. Muse framed the AI infrastructure buildout as a generational semiconductor cycle, telling investors he sees industry revenue reaching roughly $3 trillion by 2029 and potentially topping $3.5 trillion by 2030. BofA’s Vivek Arya raised his 2030 total semiconductor addressable market forecast to $2.7 trillion from $2.3 trillion, led by memory and data center, with autos and industrial recovering on top.

The logic runs through high-bandwidth memory, or HBM, which stacks DRAM chips into a single high-value package for AI accelerators. HBM needs far more testing than standard memory, so a memory boom is supposed to flow downstream into test demand. CEO Gregory Smith made that mechanism explicit at the Bank of America 2026 Global Technology Conference. Describing a DRAM headed into an HBM stack, he said the test intensity “is much higher because of the stacking and the quality requirements downstream.” The more complex and expensive the AI chip, the more it has to be tested before a failure becomes catastrophic downstream.

The number behind the bull case

Smith put a frame on the opportunity that explains why analysts will underwrite targets this high. He said the overall test-equipment market was about $9 billion in 2025 and could reach roughly $20 billion in a hypothetical environment where wafer front-end spending hits $250 billion. Inside a $12 billion to $14 billion automated test equipment market, he argued Teradyne could become a $6 billion company, roughly double its 2025 size, as its share climbs from around 30% toward 35% to 38%.

That share gain is the part bulls care about most. Teradyne lost ground from 2021 to 2025 as the market shifted toward GPU and DRAM, segments where its position was weaker. Smith said the company has since gained share inside both compute and DRAM, with mobile, power, and flash positioned to recover. As he put it, “more wafers means more test.” The case for $550 is a case that this share-and-TAM math compounds for years rather than spiking for a few quarters.

Teradyne Street Targets (TIKR)

Teradyne Street Targets (TIKR)

See historical and forward estimates for Teradyne stock (It’s free!) >>>

What the bulls are quiet about

Teradyne’s own near-term guidance points the other way. Q1 2026 was a record: revenue of $1.282 billion, up 87% year over year, with non-GAAP earnings per share of $2.56. But management guided Q2 revenue to a range of $1.15 billion to $1.25 billion, a midpoint below the Q1 actual. That is a sequential step down, and management has flagged limited visibility into the back half of the year.

The market has already shown it will punish that lumpiness. Despite the record Q1 beat, the stock fell 19.41% the day after its April 28, 2026, report as investors questioned the premium valuation, and it carved out a 26.73% drawdown on April 29. It is also worth noting that part of the recent run is mechanical: Teradyne joined the Nasdaq-100 on June 22, forcing passive funds to buy the shares regardless of valuation. And the $399 mean target lags the move, because slower analysts have not yet updated, so consensus understates current sentiment even as it sits below the price.

Valuation is where the skepticism concentrates. On EV/EBITDA, Teradyne trades at an NTM (next twelve months) multiple of around 49x. Its semiconductor-equipment peers sit well below that on the same measure: ASML at roughly 36x, Applied Materials around 40x, Lam Research near 47x, and test rival Advantest at about 32x. The premium is real across the board. The question is whether around 23% forecast EPS growth justifies it, or whether the multiple already banks the AI cycle the bulls are still describing as early.

Teradyne NTM EV/EBITDA (TIKR)

Teradyne NTM EV/EBITDA (TIKR)

See how Teradyne performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $463.21

- Model Target (Mid-Case Upside): ~$1,040

- Potential Total Return (Mid-Case): ~125%

- Annualized IRR (Mid-Case): ~20% / year

Teradyne Advanced Valuation Model (TIKR)

Teradyne Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Teradyne stock (It’s free!) >>>

A word on which case this is, because it matters. TIKR’s more conservative model run, built on near-term consensus, lands around $390, implying downside from today’s price. The figure above is the more bullish mid-case scenario, which assumes Teradyne captures the CAGR the bull thesis describes: around 19% revenue growth and around 23% EPS growth through 2030. The two outputs are far apart for one reason, and it is the same reason the analyst targets are split: everything hinges on whether the AI test cycle compounds or digests. I am showing the upside case because that is what the $550 targets are effectively pricing, and the point is to test whether it is reachable.

Two revenue CAGR drivers carry the mid case: share gains in compute and DRAM testing as AI accelerators and HBM expand test intensity, and recovery in the slower-moving mobile, power, and flash segments. The margin driver is mixed, as a richer Semiconductor Test share lifts the net income margin toward around 28%. The primary risk is customer concentration, where a single program delay can dent estimates and the multiple at once.

The upside: if the addressable market doubles toward $12 billion to $14 billion and Teradyne holds its share gains, the mid case compounds to a stock worth roughly double over the next several years.

The downside: if AI capital spending digests faster than management’s timeline implies, the conservative ~$390 path wins, the premium multiple compresses, and the concentration that drove the rally drives the reversal.

Conclusion

The disagreement resolves on July 28, 2026, when Teradyne reports Q2 after the close. Watch the full-year framing, not the headline beat. Good looks like management holding or raising full-year targets while confirming that memory and HBM orders are actually building in the backlog. Bad looks like in-line results, no raise, and more cautious back-half language that confirms the lumpiness bears.

Remember what happened last time: the stock dropped more than 19% after a record beat because guidance, not the print, set the tone. With Cantor at $550, the Street mean near $400, and the stock at $463, this is the rare setup where the reaction will tell you more than the result. Mark the date.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Teradyne?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Teradyne, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Teradyne alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Teradyne on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Conservative columnist argues: Rubio could be more dangerous than Trump

Why this former OpenAI researcher thinks it’s time to start gaming out AI’s future