‘These People Are Heroes’: Dave Ramsey Praises Couple Who Paid Off $420,000 in 10 Years

The post ‘These People Are Heroes’: Dave Ramsey Praises Couple Who Paid Off $420,000 in 10 Years appeared first on 24/7 Wall St..

- Paying off $420,000 debt over 10 years works: $40,000 credit card at 21% APR costs $8,400/year in interest; redirecting to principal pays it off in 5 years without income increase.

- High-rate debt payoff strategy (15%+ APR) fails against 50%+ employer 401(k) matches, as guaranteed match returns exceed interest savings.

- Are you ahead, or behind on retirement? SmartAsset's free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don't waste another minute; learn more here.

On a June 16 Ramsey Solutions debt-free stage segment, Scott and Kim from Applegate, California announced they had paid off $420,000 in 10 years, including credit cards, a car payment, IRS back taxes, a student loan for their son, and their mortgage. Dave Ramsey’s verdict was unambiguous: “These people are heroes. This is how it’s done right here. And so please don’t tell me you’re not willing to pay a price to win. They’re standing in front of you saying it’s worth it. Pay a price and you’ll win.”

The stakes for any reader weighing this advice are concrete. Scott described the trigger plainly: “We were doing silly things like paying off credit cards with credit cards, and just feeling the weight of it.” If you are carrying revolving balances right now, the cost of inaction is measurable, and the cost of waiting another decade to act is larger than most people realize.

The verdict: the framework works, the math is the proof

Ramsey’s core claim, that you can dig out of a six-figure hole through disciplined, sequenced payoff, is mathematically sound. The reason it works is leverage against compounding interest, and the credit card portion of Scott and Kim’s debt is the cleanest illustration.

The average credit card APR sits at around 21% currently, with the 12-month range running between 20.97% and 21.39%. Carry a $15,000 balance at 21% and pay only the minimum, and roughly $3,150 a year evaporates into interest before you reduce a dollar of principal. That is the “weight” Scott described, in literal dollars.

Scale it up. A household with $40,000 in revolving balances at 21% is funneling roughly $8,400 a year into the lender before principal moves. Redirect that same cash into the balance and the account closes inside five years even without raising your income. That mechanic, freed cash flow attacking the highest-rate debt first, is what made Scott and Kim’s household income range of $160,000 at the start to $260,000 at the end capable of erasing $420,000 in a decade. The achievement looks even sharper against the backdrop. Credit card delinquencies stood at 2.92% in January 2026, and the national savings rate has slid from 6.2% in Q1 2024 to 3.7% in Q1 2026. The typical household is moving the wrong direction.

The variable that flips the answer: interest rate

Ramsey’s framework treats all non-mortgage debt as a single enemy to be killed in sequence. The math says otherwise. The deciding variable is the rate on each individual balance.

Scenario A: a $20,000 credit card at 21% versus a 401(k) match of 50 cents on the dollar up to 6% of salary. Skipping the match to throw everything at the card costs you a guaranteed 50% return on contributions, while the card costs you 21%. The match wins. Capture it first, then attack the card.

Scenario B: a $20,000 federal student loan at 4.5% versus the same card at 21%. Here the card is roughly four times more expensive than the loan. Paying minimums on the loan while annihilating the card is straightforward optimization.

Where Ramsey is most clearly correct is the high-rate consumer debt portion of Scott and Kim’s story. Where his framework is incomplete is when low-rate debt is bundled with employer match opportunities the Baby Steps tell you to pause.

What to do this week

- List every debt by interest rate. Include the balance, minimum payment, and APR. Anything above 15% is an emergency. Anything above the 21% average is a five-alarm fire.

- Confirm your employer match before pausing retirement contributions. A 50% or 100% match is a guaranteed return no debt payoff can replicate. Capture it, then redirect everything else.

- Build a written payoff schedule. Decide between avalanche (highest rate first, lowest total interest) and snowball (smallest balance first, fastest psychological wins). Run both totals and pick deliberately.

- Automate the redirected cash flow. The moment one balance closes, the freed payment shifts to the next debt on the list the same day, not next month.

Ramsey’s closing line to Scott and Kim was “Live like no one else so later you get to live and give like no one else.” Strip the slogan and the instruction is concrete: identify the highest-rate dollar in your life, kill it first, and keep the cash flow moving up the ladder until there is nothing left to pay.

If You’ve Been Thinking About Retirement, Pay Attention (sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance, and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor. Here’s how:

-

Answer a Few Simple Questions.

-

Get Matched with Vetted Advisors

-

Choose Your Fit

Why wait? Start building the retirement you’ve always dreamed of. Get started today! (sponsor)

The post ‘These People Are Heroes’: Dave Ramsey Praises Couple Who Paid Off $420,000 in 10 Years appeared first on 24/7 Wall St..

You May Also Like

Dow Jones futures plunge as risk aversion increases after Trump’s comments

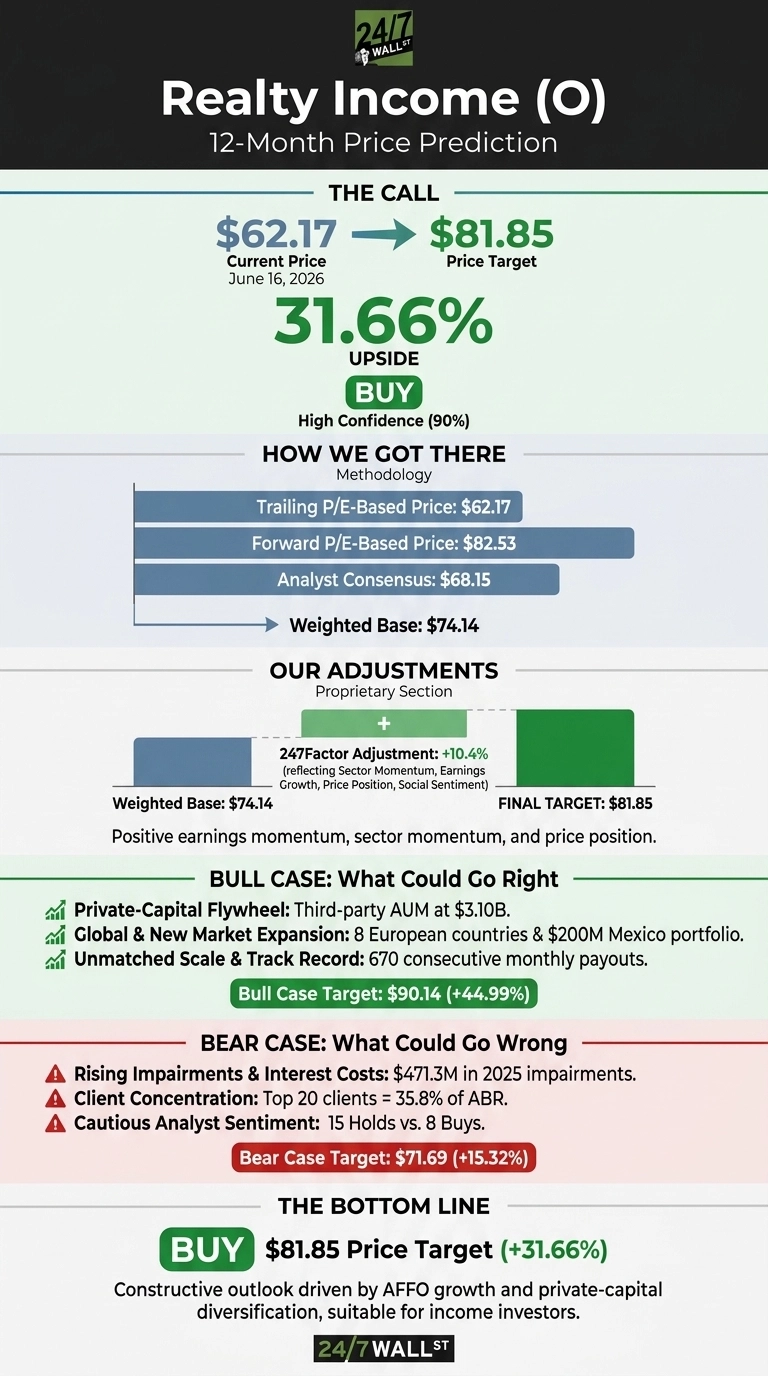

Our Highest Conviction Call on Realty Income Points to 30% Upside

Richard Harris Law Firm Partners with CCSD to Honor School Bus Drivers at Appreciation Event