You’re Picking the Wrong S&P 500 ETF and It’s Costing You Money Every Year

The post You’re Picking the Wrong S&P 500 ETF and It’s Costing You Money Every Year appeared first on 24/7 Wall St..

- VOO beats SPY due to lower expense ratio, preserving more of 8-10% annual returns over decades and turning basis points into thousands.

- Index choice matters more than fees; QQQ's tech concentration shouldn't be confused with broad-market diversification.

- Are you ahead, or behind on retirement? SmartAsset's free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don't waste another minute; learn more here.

Vivian Tu, the creator behind Your Rich BFF, spends a chunk of her Networth and Chill episode on a quiet detail most new investors skip past. “It’s a percentage that you’ll pay on top of your gains or losses,” she says about expense ratios, the fee baked into every mutual fund and ETF. If you buy the wrong fund tracking the right index, you bleed money every year you hold it, in good markets and bad. Those are the stakes here. You are picking between two cars that drive the same route, where one charges you extra tolls for no reason.

The fee math Tu is describing

Tu’s verdict is correc. An expense ratio is skimmed off your returns before they ever hit your statement.

A 0.1% expense ratio on an 8% gain means you keep 7.9%. Lose 5% in a down year and you have effectively lost 5.1%. The fee does not care which direction the market went. It shows up either way.

Now stretch that across decades. Two funds can hold the same 500 stocks, in the same weights, and deliver returns that drift apart purely because one charges more to do the exact same job. Tu’s specific call-out is SPDR S&P 500 ETF (NYSEARCA:SPY) versus Vanguard S&P 500 ETF (NYSEARCA:VOO), both tracking the S&P 500. “By choosing VOO instead, you’d save money annually while accomplishing your financial goals.” Same index. Different toll booth.

For context on what the index itself has done, SPY is up about 10% year to date and up roughly 25% over the past year. Whatever fee you pay, you pay it on top of that. A handful of basis points sounds like nothing on a $5,000 balance. On a $200,000 retirement account compounding for 25 years, the same handful of basis points turns into real money.

Where Tu’s starter list quietly trips people up

Her beginner menu has four entries, and one of them is not what people think it is. VOO for the S&P 500. QQQ for the Nasdaq-100, which she flags as “a little bit tech heavier.” Vanguard Total World Stock ETF (NYSEARCA:VT) for “everything in the world versus just the US.” And target-date retirement funds for hands-off investors.

The trap is QQQ. Invesco QQQ Trust (NASDAQ:QQQ) tracks the Nasdaq-100, a concentrated bet on large non-financial tech. That is why its returns have run hotter, up almost 19% year to date and about 37% over the past year, but it is a different risk profile. Buy QQQ thinking it is a broad-market index and you have quietly tripled down on a few names instead of owning 500. The fee question matters. The index question matters more. Tu picked the right variable to highlight, but readers should understand they are choosing the road before they negotiate the toll.

The target-date shortcut

For investors who do not want to think about any of this, Tu offers a clean rule. Figure out the year you turn 65, round to the nearest year ending in 5 or 0, and pick the fund with that year in its name. A target-date fund automatically rebalances as you age, getting more conservative on its own. The catch is the same as everywhere else. Two target-date funds aimed at the same year can charge wildly different fees, and the only way to know is to look at the expense ratio before you click buy.

What to actually do before your next contribution

- Decide what you want exposure to first. The S&P 500, the Nasdaq-100, global stocks, or a target-date glide path. The index drives almost all of your return.

- Pull up two or three funds that track the same thing. Compare their expense ratios side by side on the fund’s own fact sheet, not a third-party summary.

- Apply Tu’s math to your real balance. Take your contribution amount, multiply by the difference in expense ratios, and decide whether that annual leak is worth it.

- Confirm the money actually invested. “Make sure not to just put money into an investment account and then say you’re done. You’re not finished until your cash is actually deployed.”

Pick the index, then pick the cheapest credible fund that tracks it. The rest is patience.

If You’ve Been Thinking About Retirement, Pay Attention (sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance, and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor. Here’s how:

-

Answer a Few Simple Questions.

-

Get Matched with Vetted Advisors

-

Choose Your Fit

Why wait? Start building the retirement you’ve always dreamed of. Get started today! (sponsor)

The post You’re Picking the Wrong S&P 500 ETF and It’s Costing You Money Every Year appeared first on 24/7 Wall St..

You May Also Like

Dow Jones futures plunge as risk aversion increases after Trump’s comments

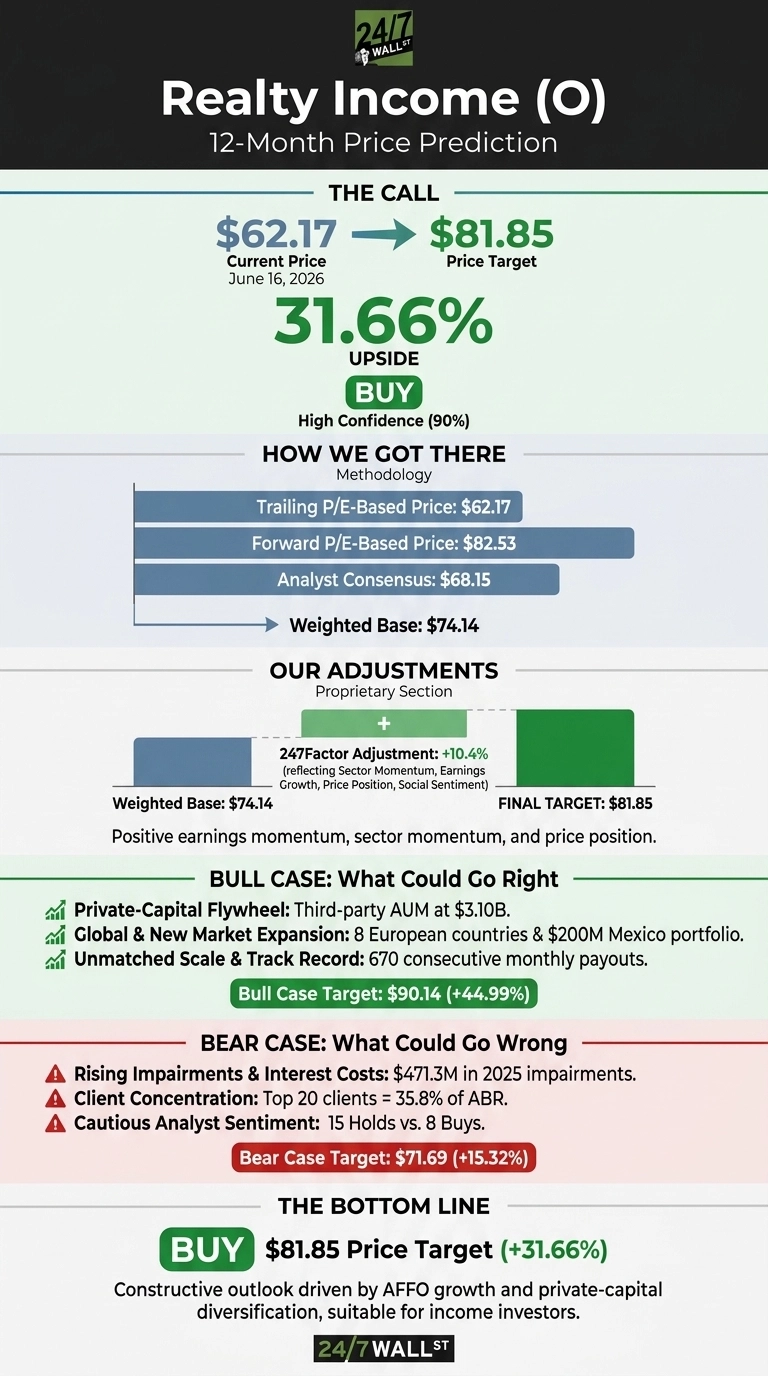

Our Highest Conviction Call on Realty Income Points to 30% Upside

Richard Harris Law Firm Partners with CCSD to Honor School Bus Drivers at Appreciation Event