What Liquidity Crises Actually Look Like Before the Crash

The crash is loud. The fragility that produces it is silent — and that is the part most traders never learn to see.

By the time a crash is visible on the chart, the conditions that made it possible have already been in place for days, sometimes weeks. The break is not the cause. The break is the moment the slow erosion finally becomes impossible to ignore.

The signals do not appear in price. They appear in how the order book behaves, how reactions form, how liquidity gets used. None of these signals look dramatic. That is precisely why they get missed.

The Difference Between a Move and a Break

Most large declines are not the result of a single decisive event. They are the result of an environment that can no longer support the structure built on top of it.

A normal sell-off pulls in buyers. Bids appear at expected levels. Reactions form. The market absorbs the supply and continues. This is what a functioning market looks like, even in a downtrend.

A pre-crash environment looks different. The same kinds of sell-offs do not pull in the same kind of response. Bids that should appear do not. Reactions that should form do not. Levels that should hold do not. Each event individually looks small. Collectively, they describe a market that has lost its ability to absorb supply.

This is the silent phase. Nothing dramatic has happened yet, but the structural conditions for something dramatic have already assembled.

Failed Reactions as a Leading Signal

A reaction is the market’s response to pressure. When sellers hit the market, buyers should step in. The strength of that response tells you something about the state of demand.

Failed reactions are the earliest warning. Price drops to a level where buying has appeared before. This time, the buying is thinner. The bounce is shorter. The recovery does not reclaim what was lost.

Then it happens again at the next level. The same pattern. Slightly weaker each time. From a price chart, this might look like a normal pullback. From an order book perspective, it is a structural change. Demand is becoming more reluctant and more conditional.

A single failed reaction is noise. Three or four failed reactions in sequence is a pattern. The pattern says that the level of conviction required to step in as a buyer has risen. Which means the level of conviction required to absorb a future shock has risen along with it.

Thinning Liquidity Underneath

Liquidity is not constant. It is provided by participants who have a reason to be in the market at a given price. When those participants step back, the same chart can look the same while behaving very differently.

In a thinning environment, the resting bids that used to sit at multiple price levels are no longer there. The depth that used to absorb sell flow is gone. The market still trades. Price still moves in orderly ranges. But the cushion that prevents sharp moves has been quietly removed.

This is hard to see on a price chart because nothing about the price tells you what is sitting in the book at lower levels. The price reflects the last transaction. The fragility reflects the absence of future transactions that would otherwise occur if pressure arrived.

A market with thin liquidity does not crash because of an unusual event. It crashes because a normal event produces an outsized reaction. The same sell flow that would have been absorbed two weeks earlier now has no cushion to land on.

This is also why positioning out before the visible move arrives carries the cost of being early — the warning signs are visible before the resolution, but acting on them means accepting a long uncomfortable window where the price has not yet confirmed what the structure already implies.

How Order Books Tell the Story

The order book is the most direct view of liquidity, and it shows what price cannot.

In a healthy market, the book has depth on both sides. Bids and offers extend across multiple levels. The size at each level is roughly symmetric. Replenishment is steady.

In a deteriorating market, the asymmetry shows up first. Bids get thinner faster than offers. Each filled bid is not immediately replaced. The depth that looks present at a glance turns out to be the same handful of orders being layered closer to the spread, not new orders adding to the cushion.

A market where the same liquidity gets recycled is structurally different from a market where new liquidity continually enters. The price chart will not distinguish between them. The book does.

Most traders never look at the book in this way. The book is treated as noise — too fast, too detailed, too local. But the texture of the book in the days before a fragile break carries information that the chart simply does not contain.

The Quiet Phase Before the Break

The phase immediately before a serious decline is usually quiet, not dramatic.

Volume is normal or below average. Volatility is contained. Price action looks orderly. The market gives no obvious signal that anything is wrong. This is the texture of a market that has lost its absorptive capacity but has not yet been tested.

This pattern of silence before the storm is consistent across crashes — the quiet phase carries the warning signs, but the warning signs do not look like warnings. They look like calm.

The reason for the quiet is structural. In a thinning environment, the participants who would normally generate volume have already reduced their activity. Market makers have widened their spreads. Long-term holders are holding. Discretionary traders are sidelined. The activity that produces noise is exactly the activity that is missing.

A quiet market is normally interpreted as safe. In a pre-crash context, the quiet is the symptom. The market is not at rest. It is depleted.

Hidden Fragility in Funding and Leverage

Beyond the order book, fragility shows up in the structure of leverage that has accumulated during the trend.

When a trend has extended, leverage tends to be one-sided. Open interest grows in the direction of the move. Funding rates tilt. The cost of holding aligned positions becomes a slow tax that quietly increases the sensitivity of the entire system.

This does not need to be visible to be active. A leveraged structure can sit for weeks without consequence. It only matters when something else moves first. A small decline triggers liquidations. The liquidations become forced selling. The forced selling hits a market that has already thinned. The thinned market produces an outsized move. The outsized move triggers the next round of liquidations.

This cascade is the actual mechanism of a crash. The catalyst is rarely large. The fragility was already complete.

Funding rates and open interest, like the order book, tell a story that price does not. They describe the conditions under which a small event can produce a large outcome.

Why Most Traders Miss This

The signals are not hidden. They are simply not where most traders look.

Traders focused on price look at price. Traders focused on indicators look at indicators. Both of these are downstream of the conditions that produce moves. By the time price or indicators confirm what is happening, the cushion is gone.

The other reason these signals are missed is that they require negative interpretation. A failed reaction is the absence of an expected response. Thinning liquidity is the absence of expected depth. A quiet pre-crash market is the absence of normal activity.

The human attention system is built for events, not for non-events. It is easier to notice a candle that prints than a bid that did not appear. It is easier to react to a headline than to register the absence of one. Negative space is harder to perceive than presence, and most fragility lives in negative space.

This is the central asymmetry. The information is there, but the format of the information does not match the format of normal attention.

How Crashes Resolve What Was Already True

When the visible decline arrives, it does not introduce new conditions. It expresses conditions that were already present.

The participants who get caught are not punished for failing to predict the future. They are caught because they treated price as the primary data source, and price was the slowest variable in the system. The order book moved first. Reactions weakened first. Liquidity thinned first. Price was the last surface to break, because price is what every other variable eventually has to confirm.

This is why post-crash analysis often surfaces obvious warning signs. The signs were obvious only in hindsight because hindsight removes the requirement to weight evidence in real time against a chart that still looked fine.

The market is not deceiving anyone. It is operating exactly as it always has. The information is published continuously, in formats most participants are not reading.

Reading Fragility as a Habit

Fragility is not a setup. It is a state. You do not catch it by watching for a specific pattern. You catch it by developing a habit of reading the texture of the market underneath the price.

Are reactions forming where they should? Is depth being replenished or recycled? Is volume normal or hollow? Is funding extended? Is leverage one-sided? Is the market behaving like a market that can absorb a shock, or like a market that cannot?

None of these questions produce a binary signal. They produce a slowly shifting impression of structural health. That impression is what tells you whether the next sell flow will be absorbed or amplified.

The crash is loud because all of these conditions resolve at once. The fragility is silent because each condition only matters in combination, and combinations do not have visible shapes.

Most traders learn to see the crash. The harder discipline is learning to see the fragility, in the days before, when nothing on the chart is asking for attention and the market still looks like every other market that did not break.

More from SwapHunt

Long-form observations on structure, behavior, and timing.

Free download: The Cost of Being Early — On positioning before the market moves.

Ebooks:

📘 Quiet Edges — On tempo, structure, and optionality

📗 Reading the Market, Not the News — On structure, behavior, and second-order effects

📙 When Not to Trade — On decision-making under uncertainty

Follow @SwapHunt for daily observations.

This content is for educational purposes only. Not financial advice.

What Liquidity Crises Actually Look Like Before the Crash was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.

Ayrıca Şunları da Beğenebilirsiniz

Shiba Inu Sees 4.8B SHIB Exchange Inflows as April Starts Weak

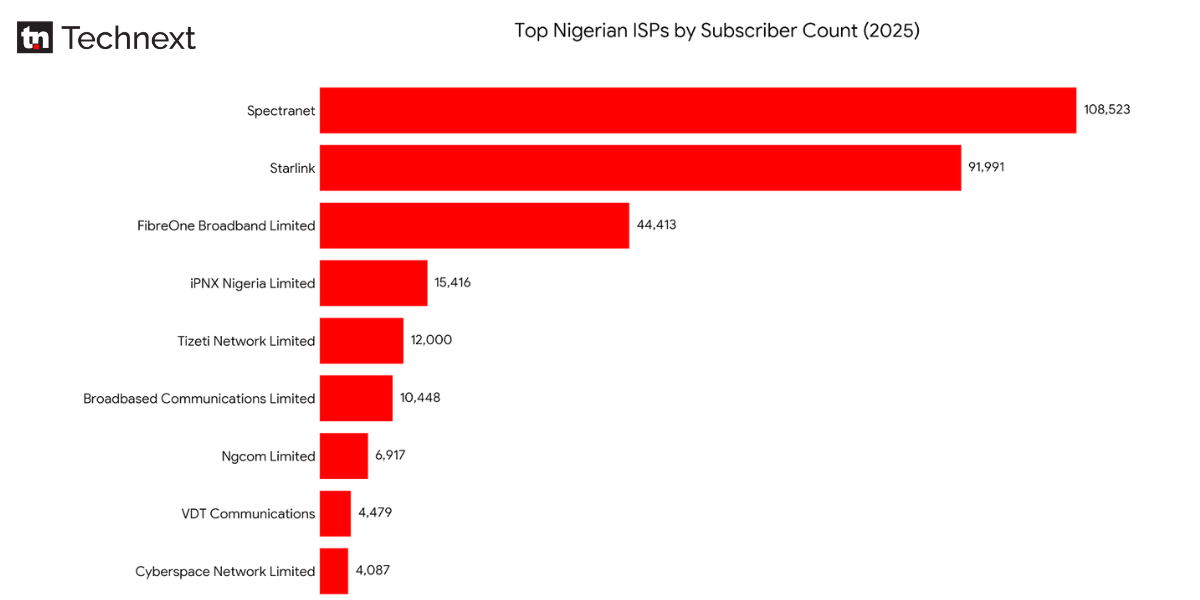

Spectranet returns to 100k-subscriber mark as Nigerian Internet Service Providers end 2025 with 352k users

How Mutuum Finance (MUTM) Builds Long-Term Value in Cheap Crypto Markets

Popüler Haberler

Daha fazla