The Augusta Rule: Rent Your Own House to Your Business for 14 Days a Year Completely Tax-Free

The post The Augusta Rule: Rent Your Own House to Your Business for 14 Days a Year Completely Tax-Free appeared first on 24/7 Wall St..

If you own a home and run a business, the IRS will let you rent your house to that business for up to 14 days a year and pocket every dollar tax-free. No reporting. No Schedule E. No income tax on the rent. This is the Augusta Rule, and it has been quietly sitting inside the tax code since 1976, mostly used by Masters Tournament homeowners in Augusta, Georgia who rent their houses to golf fans for a week. You can use the same loophole.

The buried benefit, in one paragraph

Here is the rule. If you rent your personal residence for fewer than 15 days during the calendar year, the rental income is excluded from your gross income. Completely. Meanwhile, the renter, including your own business, can still deduct that rent as an ordinary business expense. So your S-corp or LLC pays you fair-market rent for a board meeting, a strategy retreat, a client dinner, or a video shoot at your home. The business writes off the cost. You receive the cash and owe zero federal income tax on it.

The proof: Section 280A(g)

The authority is Internal Revenue Code Section 280A(g), sometimes called the “14-day rental rule” or “Masters exception.” The statute says that if a dwelling unit is used as a residence and is rented for fewer than 15 days during the taxable year, no rental income is included and no rental deductions are allowed. IRS Publication 527 (Residential Rental Property) restates the same rule in plain English. It has not changed for 2026.

Who qualifies, who doesn’t

You qualify if you own a home (primary or secondary) that you personally use as a residence, and you have a legitimate business that can legitimately use the space. The cleanest fit is an S-corp, C-corp, partnership, or multi-member LLC, because those are separate taxpayers from you. A pure sole proprietor filing on Schedule C cannot use this trick, because you cannot rent property to yourself. Renters and people who already claim a home-office deduction for the same square footage face complications and should tread carefully.

How to actually use it in 2026

- Confirm a real business purpose. Quarterly board meetings, annual planning retreats, team training days, client events, or a recorded podcast/video shoot all work. A fake meeting will not.

- Set a fair-market rent. Get three written quotes from local hotels, conference centers, or short-term venues of comparable size. Save the screenshots. The IRS expects the rate to look like what an arm’s-length renter would pay.

- Sign a written rental agreement between you (the homeowner) and your business, listing date, hours, purpose, and rent.

- Keep meeting minutes or an agenda proving the business actually used the home that day.

- Have the business pay you by check or transfer. Do not pay cash.

- Track the days. Stop at 14 rental days in the calendar year. Day 15 detonates the whole strategy.

- Report it correctly. The business deducts the rent on its return. You do not report the income on your Form 1040. If the business issues a 1099, list the gross on Schedule E and back it out with an offsetting Section 280A(g) adjustment so the IRS computer matches.

The catch

Hit 15 days and you lose everything. All the rent becomes taxable, and the home is reclassified as a rental property for the year, dragging in depreciation recapture headaches. The rent also has to be defensible. Charging your S-corp $5,000 a day for a meeting in a $300,000 house will get disallowed in an audit, and Tax Court cases (Sinopoli v. Commissioner, 2023, among others) have already slashed inflated Augusta deductions. Sole proprietors and single-member LLCs taxed as disregarded entities cannot use it at all. And the home must qualify as a residence, meaning you personally used it more than 14 days or 10% of rental days, whichever is greater. Document everything: agenda, attendees, comparable rates, invoice, payment. If you cannot prove it on paper, you cannot defend it.

Don't wait: the analyst who called NVIDIA in 2010 just revealed his top 10 AI stocks. See the full list FREE now.

The post The Augusta Rule: Rent Your Own House to Your Business for 14 Days a Year Completely Tax-Free appeared first on 24/7 Wall St..

Potrebbe anche piacerti

Dow Jones futures plunge as risk aversion increases after Trump’s comments

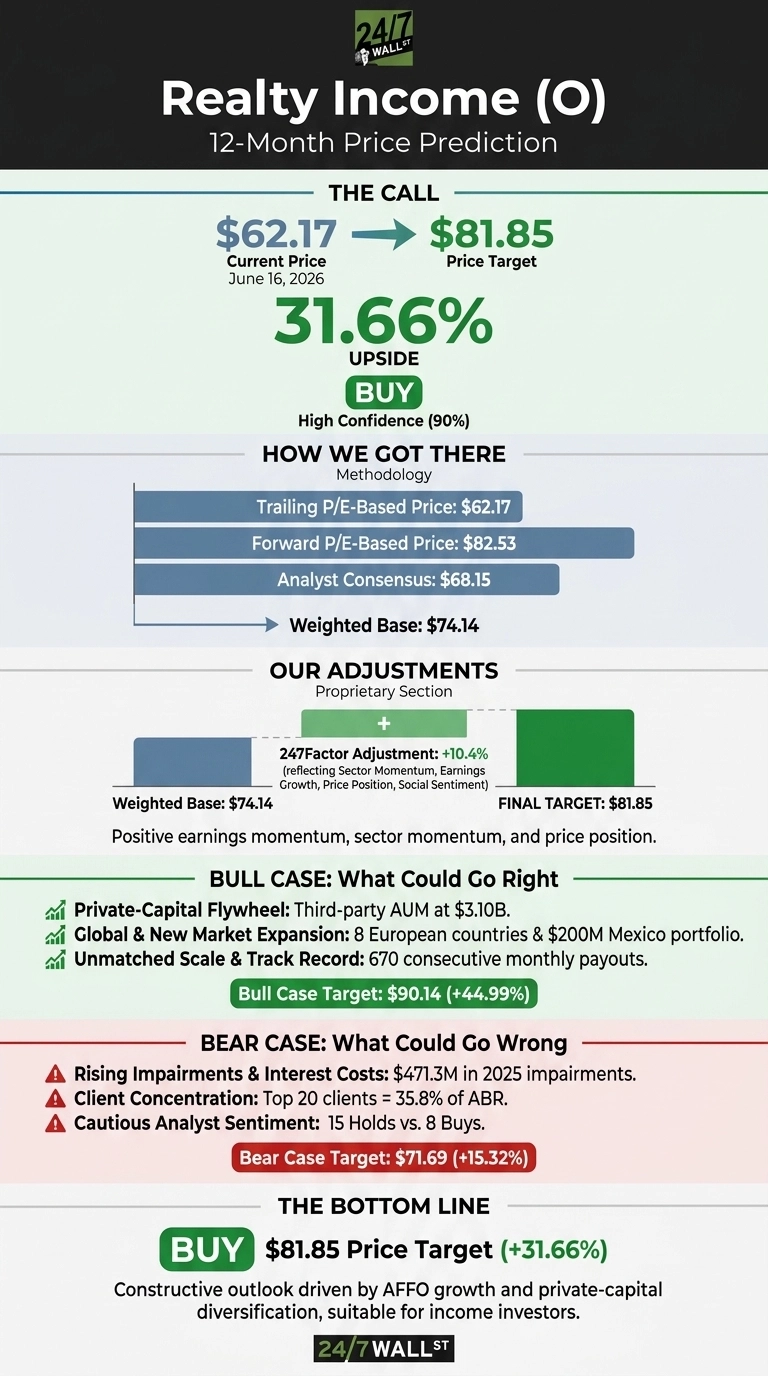

Our Highest Conviction Call on Realty Income Points to 30% Upside

Richard Harris Law Firm Partners with CCSD to Honor School Bus Drivers at Appreciation Event

Notizie di tendenza

Altro